Discounting expected cash flows is used when. Evaluation of investment projects using discounted cash flows. Discounting cash flows. Definition

This article is devoted to the calculation of the main indicators of the effectiveness of investment projects, calculated taking into account the time factor, as well as to the issues arising in the calculation of indicators. The article is aimed at specialists of financial and economic services, who, perhaps for the first time, are faced with the task of assessing investment project, in order to provide results to the owner of the company, to attract third-party investors or creditors.

To evaluate investment projects, two groups of indicators are used: indicators calculated without taking into account the time factor and indicators calculated taking into account the time factor.

The first group of indicators is easier to calculate, but it does not take into account the fact that today's and tomorrow's money for the investor costs differently, that is, the calculations of these indicators are carried out without bringing the cash flows to a single point in time.

The second group of indicators, about which and there will be a speech in the article, in contrast to the indicators of the first group, they take into account the different value of money at different points in time (the theory of the time value of money). These indicators are more interesting for owners, investors and banks, since they more correctly reflect the effectiveness of the project (they do not overestimate it, as the indicators of the first group), that is, they are a more reliable (better) guarantor of the project's success. The essence of their calculation is to bring future cash flows (value of money) to "today", or rather, to the time of the start of investment in the project (it is assumed that the investment will be made this year). Bringing cash flows is called discounting, the essence of which is that "today" we need to decide whether to invest in a project, or there is a problem of choosing a more efficient project from several, for this it is necessary to know: how profitable or not profitable project; or which project is more efficient (profitable)? To do this, we draw up a business plan - we model the activity for several years in advance in order to calculate efficiency, and we model it based on “today's” prices, expenses, estimated income (and, accordingly, based on “today's” payments and receipts). We should also take into account alternative risk-free investments, which could bring us a certain income for sure, the risks of an unfavorable outcome of the project, the required rate of return on invested capital. It is assumed that it is precisely the discounting of the planned cash flows that brings them to the current moment, taking into account inflation, risk-free investments, the risks of a particular project, or the required rate of return on invested capital, depending on the chosen approach to determining the discount rate used when discounting cash flows. The results of discounting and assessing the effectiveness of the project largely depend on the discount rate, which in turn depends on the method of its determination (calculation).

The choice of the option for determining (calculating) the discount rate is a separate large topic, which has been described more than once in various sources - the Internet, textbooks, books, in specialized magazines. Therefore, we will not dwell on it in detail, I will only note that there are several approaches to determining the discount rate, such as:

- Determination of cost equity capital(CAMP long-term asset valuation model);

- Weighted average cost of capital (WACC);

- Cumulative construction is the most commonly used approach based on expert risk assessment.

- NPV - pure discounted income(net present value of the project);

- IRR - internal rate of return (profit / return) of investments;

- DPBP - discounted term return on investment

The calculation of indicators is carried out on the basis of data from the movement plan Money an investment project, which in turn is built on the basis of a plan of income and expenses of the project and a schedule of receipts and payments. Thus, it is important that the initial information for modeling activities within the planning horizon (the project period under consideration), as well as the plans for the movement of funds, income and expenses themselves, are as developed, accurate and correct as possible, in order to minimize the error in the calculation results and risks. project. This raises the question: should inflation be taken into account when modeling activities and how to do it? There are two ways to take inflation into account in calculations:

- Deflation of cash flows before discounting, that is, by modeling cash flows taking into account inflation for the periods of the project, for example, adjusting the amounts for the inflation coefficient;

- Taking into account the inflationary component when calculating the discount rate

The question often arises: what is the project term (planning / research horizon of the project) and how to determine it, because the longer the term we consider, the greater the value of the main project performance indicator (NPV)? Theoretically, the planning period of a project should be equal to the life cycle of the project, that is, the time interval from the moment of its appearance (start of investment) to its liquidation / complete wear and tear. But imagine if you are considering a project with a life cycle of more than 10 years. Does this mean that we have to model activities for more than 10 years in advance? This is quite difficult in today's economic environment. Therefore, you should model the activity for a period that allows you to more accurately and confidently plan the cash flows, income and expenses of the project (several years), but the period should be at least simple term payback of the project, so that it is possible to calculate the discounted payback period of the project. If a project with 100% credit financing is considered, it is recommended to consider the project term equal to the loan maturity (number of years). The planning period can be understood directly in the process of modeling - the formation of a cash flow plan. However, a common mistake when evaluating investment projects when the planned period is shorter life cycle the project and the calculation of indicators does not take into account the residual / liquidation value of the project, which can significantly reduce the value of performance indicators. The residual / liquidation value of the project must be taken into account in the calculations for the purpose of their correctness.

The project period is usually a year, since the traditional discounting formula implies discounting cash flows by years, thus, in the case when the project period is not a year, the discount formula will need to be adjusted, or the discount rate itself should reflect not an annual, but a monthly difference in value of money.

Now let's turn directly to the performance indicators of the investment project, calculated taking into account the time factor. For clarity, we will consider the calculation methodology using an example. As an example, let us take a project for the construction of a non-residential real estate object at 100% of borrowed funds ( credit line). It is planned to receive income from the sale and lease of the area of this property.

Table 1 shows a simulated cash flow plan for this project. The considered project period is 7 years, in which it is possible to plan income and expenses more accurately and which is longer than the simple payback period of the project. In the 7th year of the project, the proposed liquidation cash flow(residual value of the property minus income tax) with a "+" sign from the simulated sale of the property at the end of the considered project period.

Table 1

| 1 year | 2 year | 3 year | 4 year | 5 year | 6 year | 7 year | |

| Balance at the beginning of period | 0 | 3 784 778 | 29 157 938 | 70 496 191 | 106 072 147 | 141 618 389 | 257 390 934 |

| Receipts | 590 833 375 | 479 124 033 | 434 469 792 | 392 763 800 | 470 343 200 | 476 512 400 | 476 434 800 |

| Credit funds | 566 800 000 | 177 700 000 | 0 | 0 | 0 | 0 | 0 |

| Income from sale, lease | 24 033 375 | 301 424 033 | 434 469 792 | 392 763 800 | 470 343 200 | 476 512 400 | 476 434 800 |

| 0 | 0 | 0 | 0 | 0 | 0 | 485 346 090 | |

| Payments | 587 048 597 | 453 750 873 | 393 131 538 | 357 187 844 | 434 796 958 | 360 739 855 | 209 351 247 |

| 516 923 255 | 224 997 745 | 0 | 0 | 0 | 0 | 0 | |

| 13 354 092 | 84 974 378 | 109 391 538 | 125 960 344 | 187 744 458 | 206 367 355 | 209 351 247 | |

| % on loan (15% per annum) | 56 771 250 | 105 278 750 | 95 240 000 | 65 227 500 | 40 652 500 | 9 272 500 | 0 |

| Repayment of the "loan body" | 0 | 38 500 000 | 188 500 000 | 166 000 000 | 206 400 000 | 145 100 000 | 0 |

| Balance at the end of the period | 3 784 778 | 29 157 938 | 70 496 191 | 106 072 147 | 141 618 389 | 257 390 934 | 524 474 487 |

Traditionally, examples are given where, during the investment period, there are no payments for current expenses and the receipt of income. In our example, during the investment period, both income and operating expenses appear, and investments are made during the first two periods of the project.

So, the indicators calculated taking into account the time factor imply preliminary discounting (reduction) of the net cash flow. Net cash flow (NCF) - the difference between the amounts of receipts and payments of the company's funds for a certain period of time; calculated taking into account payments, dividends and taxes. It follows from the definition that we should deduct payments by project years from receipts and discount this flow, but there are many different opinions about what to include or not to include in the discounted net cash flow. Discussions mainly concern the flow of funds on loans, that is, the receipts of funds on the loan, the return of the “loan body” (the principal amount of the loan) and interest on it. The fact is that obtaining and repaying a loan, including interest on a loan, refers to financial activities, and to assess the effectiveness of an investment project, only the amount of investment in the project and the data of current activities are used. Therefore, we do not include in the discounted cash flows receipts and payments on loans (including interest) related to financing activities.

Under investment in in this case we mean the amount of money required for design work and the construction of a property, the purchase of fixed assets for its further operation, as well as the initial working capital required to cover operating costs during the initial operation of the facility until the proceeds cover operating costs.

The zero period of the project will be the first year of the project, then - in order (1-6 period). Table 2 shows the calculation of the net cash flow (NCF) of our project, where NCF is the difference between receipts and payments, including investments.

For reference: The question of including depreciation in the calculation of cash flows arises when indirectly determining the amount of cash flow, that is, through the plan of income and expenses.

table 2

| Project period | 0 | 1 | 2 | 3 | 4 | 5 | 6 |

| Receipts | 24 033 375 | 301 424 033 | 434 469 792 | 392 763 800 | 470 343 200 | 476 512 400 | 961 780 890 |

| Income from sale, lease | 24 033 375 | 301 424 033 | 434 469 792 | 392 763 800 | 470 343 200 | 476 512 400 | 476 434 800 |

| Income from the sale of a property (liquidation CF) | 0 | 0 | 0 | 0 | 0 | 0 | 485 346 090 |

| Payments | 530 277 347 | 309 972 123 | 109 391 538 | 125 960 344 | 187 744 458 | 206 367 355 | 209 351 247 |

| Payments for design, construction and installation work, purchase of fixed assets (investments, excluding working capital) | 516 923 255 | 224 997 745 | 0 | 0 | 0 | 0 | 0 |

| Payments for current activities | 13 354 092 | 84 974 378 | 109 391 538 | 125 960 344 | 187 744 458 | 206 367 355 | 209 351 247 |

| Net Cash Flow (NCF) | -506 243 972 | -8 548 090 | 325 078 254 | 266 803 456 | 282 598 742 | 270 145 045 | 752 429 643 |

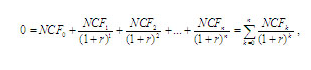

You can now discount Net Cash Flow (NCF). The discounting formula is as follows:

PVk - the present (current) value of the cash flowk-th period of the project

NCFk - Net Cash Flowk-th period of the project

k - project period

According to the discounting rule, the zero period of the project (the first year) is the investment period, we are faced with the task of bringing the net cash flows of the project to the period of the first investments in the project, that is, to the zero period, therefore, the net cash flow of the zero period is not discounted. It should be noted that in addition to investments, as mentioned above, in the zero period of the project, we have current expenses and income, which we also do not discount. The liquidation cash flow from the sale of the property at the end of the project period under consideration is discounted in the NCF of the 6th period, thereby simulating the sale of the property in the 6th project period.

For reference: there is no difference - first discount receipts and payments separately, and then calculate the discounted net cash flow (NPV) by subtracting discounted payments from discounted receipts by years, or first calculate the net cash flow (NCF = receipts - payments by years), and then discounting the net cash flow by years, the result will be the same.

Suppose that the discount rate of our project determined by the cumulative method is 20%, that is, r = 0.2. We discount the net cash flow (NCF) of 1-6 periods from table 2. Substituting the corresponding values into the discount formula, we get:

Table 3

| Project period | 0 | 1 | 2 | 3 | 4 | 5 | 6 |

| Zero Period Net Cash Flow (NCF0) | -506 243 972 | ||||||

| Discounted Net Cash Flow (PV) | -7 123 408 | 225 748 787 | 154 400 148 | 136 284 115 | 108 565 235 | 251 987 165 | |

| Accumulated discounted net cash flow | -506 243 972 | -513 367 380 | -287 618 593 | -133 218 445 | 3 065 670 | 111 630 905 | 363 618 070 |

In the case of discounting cash flows "manually" using Excel, you can use a formula created "manually":

Now let's calculate the first indicator of the efficiency of an investment project - NPV (Net Present Value) - the net present value of the project. The classic formula for calculating NPV is as follows:

NPV - net present value

NCF - net cash flow of the corresponding period of the project

k - project period

r - discount rate (in decimal)

In the case of calculating NPV using Excel, you can use the formula specially designed for this:

= NPV (rv %; cell referenceNCF1period; NCF2period; NCF3period; …; NCFnperiod) + NCF0 period*

The NPV indicator is the summation of the discounted net cash flows (PV) from 1 to the n-th period of the project and adding to it the negative cash flow of the 0-th period (investment). That is, due to the positive or negative sign of the net cash flow of each period, when calculating NPV, we add or subtract, respectively, the discounted cash flow of each next period.

According to the data from table 3 of the considered example, we get:

NPV = PV1period + PV2period +… + PV6period + NCF0 = - 7 123 408 + 225 748 787 + 154 400 148 +

136 284 115 + 108 565 235 + 251 987 165 - 506 243 972 = 363 618 070 (see the amount of accumulated net cash flow in the 6th period of Table 3)

By general rule if NPV> 0, then the project is accepted. A positive value of NPV means that the project's cash flow for the period under consideration at fixed rate of discounting covered investments and operating costs with its receipts, that is, provided min income specified by the discount rate (r), equal to income from alternative risk-free investments and income equal to the value of NPV.

When NPV = 0 - the project is neither profitable nor unprofitable, it only covered its investments and operating costs, provided min income specified by the discount rate (r) at the indicated risks. In this case, during the implementation of the project, the income of the owners will not change, but the value of the company will increase by the amount of investment.

If NPV< 0, это значит, что проект в рассматриваемый период не обеспечил даже min доход, равный доходу от безрисковых вложений, заложенный в ставке дисконтирования, а, возможно, не покрыл даже инвестиции и текущие затраты (когда чистый денежный поток проекта NCF<0).

When considering several projects, choose the one with the higher NPV.

In our case, the NPV indicator> 0, that is, the project must be adopted, but before drawing conclusions about the effectiveness of the project under consideration, the remaining indicators should be calculated and considered in aggregate.

Consider the following indicator of the effectiveness of an investment project, calculated taking into account the time factor - IRR (Internal Rate of Return) - the internal rate of return. This indicator, in contrast to NPV, reflects the profitability of the project in relative terms (in percent), therefore it is more understandable. IRR is the value of the discount rate (r) at which NPV = 0, that is, at which the present value of the proceeds is equal to the present value of the investment and current costs. IRR reflects the project's break-even rate of return, that is, when the project becomes neither profitable nor unprofitable.

To calculate this indicator, you can apply technically complex mathematical calculations using the NPV formula:

NCF- net cash flow of the corresponding period

r - discount rate (in decimal)

n - research horizon, expressed in planning intervals (project duration)

k - project period

In this case, the discount rate (r) reflects the internal rate of return (IRR).

You can calculate the IRR value "manually" by fitting (substituting) the discount rate (r) in the NPV formula until NPV = 0 is reached,

Considering our example, with a discount rate (r) equal to 20%, the NPV value has a fairly good value (363 618 070), therefore, in order to find the IRR value, let's try to increase the discount rate to 30%. Accordingly, with (r) equal to 0.3, using the same formulas as when calculating NPV with a discount rate of 20%, we obtain the value NPV = 128 563 580. The NPV value turned out to be greater than zero, but already much less, respectively, we will try to further increase the rate discounting up to 40%, we get NPV = -25 539 469. The NPV value turned out to be negative, respectively, the IRR value of this project is between 30% and 40%, closer to 40%. Thus, continuing the selection of the discount rate (r), we found the value (r) at which NPV is equal to zero - the IRR value of the project under consideration = 38%.

When calculating indicators using Excel, you can use a specially designed formula for calculating IRR:

The project is accepted when the value of the IRR indicator> discount rate (r). In this case, the project pays off the costs, provides a profit specified by the discount rate and provides a margin of profit in absolute value equal to NPV, and in relative value equal to (IRR-r). When IRR<ставки дисконтирования (r), проект следует отклонить, так как он не только не обеспечивает дополнительную доходность (запас прибыли), но даже не обеспечивает прибыль, заданную ставкой дисконтирования - минимальный доход, равный вложениям в альтернативные проекты.

Already the second indicator meets the established requirements, but do not rush to conclusions, we will calculate the next indicator.

Let's calculate the discounted payback period for our project - DPBP (Discount Payback Period), which takes into account the different cost of money over time. The discounted payback period of the project is calculated similarly to the normal payback period, the only difference is that discounted net cash flow is used to calculate the discounted payback period. The DPBP indicator reflects for what period of time the project's revenues will recoup the investment and will cover the current costs, that is, when the discounted net cash flow accumulated over the periods (years) of the project changes sign from minus to plus and will no longer change. Accordingly, the discounted payback period of the project will always be longer than the usual payback period. In our example, the accumulated discounted cash flow (see table 3) has the last negative value in the third period of the project. Usually, in the investment projects under consideration, income generation begins after the zero period of the project - in the first, therefore, the payback period starts from the first period of the project. In our case, income generation and current expenses are already present in the zero period of the project, so we will start the payback period from the zero period of the project, that is, the project period + 1 year. Thus, the discounted payback period of our project is (3 period + 1) four full years. In order to more accurately calculate the discounted payback period, we need to understand: for what part of the next (for the 4th year of the project, that is, for the 3rd period) the project will come to zero, that is, the investment will pay off completely. To do this, we divide the negative balance of the third period (133,218,445) by the value of the discounted net cash flow of the next period (PV4 = 136,284,115), we get a value of 0.98, which corresponds to 11.7 months. Accordingly, the discounted payback period of our project is almost five years, more precisely - 4 years 11.7 months.

An analysis of its sensitivity is mandatory in evaluating an investment project. The concept of sensitivity speaks for itself, its essence is that it is necessary to understand: how the project reacts to changes in certain initial data, that is, how much our performance indicators will change when the project conditions change. Sensitivity shows the strength of the project. To do this, it is necessary to select several fundamental factors that ensure the success of the project, for example:

- Demand (sales plan);

- Terms of construction and commissioning of the facility;

- The cost of design and construction and installation works (construction and installation works), etc.

- demand in terms of sales, accordingly, incomes, the amount of cash receipts and the amount of required investments will change;

- the terms of construction and commissioning of the facility, the project implementation schedule will change accordingly - expenses, incomes, payments and receipts, as well as the need for investment funds, will shift in time;

- the cost of project and construction and installation works, the costs, the amount of payments and the amount of required investment funds, etc. will change accordingly.

In our example, we will change the discount rate (r). It makes sense to change the discount rate within the IRR value. Thus, the sensitivity analysis of the project is as follows:

The considered indicators are close in nature, therefore, for one project, their ratios are fulfilled:

when NPV> 0, then IRR> r;

when NPV<0, то IRR

when NPV = 0, then IRR = r;

Now you can compare all the calculated indicators and, using the sensitivity analysis of the project, draw conclusions about its effectiveness.

The project has very good NPV and IRR indicators. The project is quite risky, as indicated by the high discount rate (r), but despite this it has a good margin of safety, that is, even with an increase in the discount rate to 38%, we have a positive NPV. The payback period of the project is five years, that is, it is a long-term investment. If this project is considered as a long-term investment, then this project should be accepted. If the project is considered with the aim of quickly making a profit with its subsequent investment in another project, that is, as a "push" project, then the payback period is quite long, that is, the project does not achieve its goals. In this case, it is proposed to try to reduce the scale of the project, that is, to reduce the initial construction area, respectively, the need for investments and operating costs will change, but incomes will also decrease. Despite this, it is possible that the scale-down of the project will satisfy its objectives.

If several alternative projects are being considered, the performance of the projects should be compared to select the best one. In any case, it is necessary to correlate them with the terms of the project - the terms of financing, risks, industry, goals and objectives of the project.

Gray fields in the formula should be replaced with the corresponding values, or with references to cells with the corresponding values

The discounting method is based on an economic law that reflects the essence of the method and describes the diminishing value of money. According to this law, over time, money gradually depreciates (loses its value) in comparison with its current value. Other changes can occur with the value of money. In order to take into account the process of such a change in calculations (for example, when calculating the potential economic efficiency of an investment), the process of such a change must be taken as a starting point, and then the size of future cash flows (inflow and outflow of funds) should be brought to the present moment, having determined the amount of change in the value of money.

Discounted Cash Flow is just a calculation that allows you to do this using a discount factor. How to calculate discounted cash flow will be shown in the article.

DCF value

The English phrase Discounted Cash Flow, meaning discounting, is usually presented in formulas in the form of the abbreviation DCF or, in the Russian version, - DCF. An investor deciding on the most profitable investments uses this result in a number of other methods representing a profitable approach to more accurately predict the future situation and choose economic and financial strategies. Among them:

- NPV- the method of net present value (NPV). The formula for its calculation, similar to the DCF formula, differs in that the initial investment costs are also included in the NPV.

- IRR Is the internal rate of return.

- NUS- the equivalent of the annual rent.

- PI- profitability index.

- NFV Is the net future value.

- NRR Is the net rate of return.

- DPP- discounted payback period.

So, for example, the introduction of the DCF parameter into the formulas for calculating the payback period (DPP) makes the calculation results almost more reliable, since it is the change in the value of money over time that makes it possible to assess the overall prospects of the project in motion. Due to the fact that the movement factor is taken into account in assessing the effectiveness of investment projects, such methods are also called dynamic.

Discounting methods are included as components of the income approach, and as such help to calculate the total value of the business and its potential. Even with the volatility of financial flows, the discounted cash flow method is justifiably applicable, since it demonstrates high accuracy. To improve the accuracy, the calculation is carried out taking into account the specific characteristics and methods of receiving funds.

However, the Discounted Cash Flow Method also has drawbacks. Among the main, most often, two are named:

- Changes in the economic, political, social environment affect the discount rate, but it is always difficult to predict changes in this rate for any long period.

- It is also difficult to predict changes in the size of future cash flows, taking into account all external and internal circumstances.

Nevertheless, the method is actively used if there is a possibility that the profitability of future financial flows will begin to differ from the profitability at the moment, if the flows depend on seasonality, if a construction project is underway, and in a number of other cases. In order to bring to the current moment the net cash flow (NPF) is used.

Discounted Cash Flow Formula

The ratio is needed to bring the potential profitability to the present value. For this, the value of the coefficient is multiplied by the value of the flows. The coefficient itself is calculated according to the following formula, where the letter "r" denotes the discount rate (it is also called the "rate of return"), and the letter "i" in the power value - the time period.

where, in addition to the previous designations, "CF" - means cash flows in time periods "i", and "n" is the number of periods in which financial flows are received.

Cash Flow (CF) in appraisal practice means:

- taxable profits

- net operating income,

- net cash flow (excluding the costs of reconstruction of the facility, operation and land tax).

The calculation algorithm involves the passage of several stages, including the analysis of discounted cash flow.

- Determination of the period for forecasting. As a rule, a predictable period of time with stable economic growth rates is forecasted. In countries with a well-developed market economy, it is 5-10 years. In domestic practice, a period of 3-5 years is traditionally considered.

- Forecasting incoming and outgoing cash payments. This is done through retrospective analysis based on financial statements (if any), studies of the state of the industry, market characteristics, etc.

- Discount rate calculation.

- Cash flow calculation for each time period.

- Bringing the received flows to the initial period by multiplying them by the discount factor.

- Determination of the total value - the stage at which the total accumulated discounted cash flow is calculated.

The key parameter in the formula is the rate. It determines the rate of return that an investor investing in a project should expect. The amount of the bet depends on a number of factors:

The key parameter in the formula is the rate. It determines the rate of return that an investor investing in a project should expect. The amount of the bet depends on a number of factors:

- weighted average cost of capital,

- inflationary component,

- additional rate of return for risk,

- return on risk-free assets,

- interest on bank deposits,

- and etc.

There are several methods for its assessment in investment analysis. The most popular methods for calculating the discount rate are shown below.

The methods differ in different approaches, each of which has specific advantages and disadvantages.

- CAPM model capital asset valuation, introduced in the 70s by W. Sharpe to determine the return on shares. The strength of the model is considered to take into account the relationship between market risk and stock returns. In the original model, this factor was the only one taken into account. Transaction costs, stock market opacity, taxes and other factors were not taken into account. Later, to increase the accuracy, Y. Fama and K. French applied additional parameters.

- Gordon's model... Its other name is the Continuous Growth Dividend Model. The “disadvantage” of the method is that it is applicable only if the company has ordinary shares with constant dividend payments, and the “plus” is in the relative simplicity of the calculation.

- WACC model- the weighted average cost of capital. One of the most popular methods for demonstrating the rate of return that needs to be paid for an investment portion of capital. The economic sense of the method is in calculating the minimum allowable profitability (profitability level). This result can be applied to the evaluation of investments in an existing project.

- Risk premium assessment method... The method uses additional risk criteria that are not provided for in other models. However, this assessment is subjective, which refers to the disadvantages of the method.

- Expert judgment method... Among the advantages are the ability to take into account non-standard risk factors and fine-tuning the analysis. Among the disadvantages is the subjective perception of the situation. The expert evaluates the meso-macro and micro-factors that, in his opinion, will affect the profit margins. Each project will have its own specific set of significant risks.

There are a number of other simple and complex methods, but in the following example, the discount rate will be calculated for clarity and transparency of the main formula as the sum of the "risk-free rate" and the "risk premium". The first component of the equation - the risk-free rate - in the example of the calculation is equal to 15% - the key rate of the Central Bank of the Russian Federation. This is part of the return on the risk-free asset. The second component - the risk premium - is set by an expert method in the amount of 8% based on a conditional assessment of production, innovation, social, technological and other risks. This is the rate of return on existing risks. In total, the discount rate will be considered equal to 23%.

There are a number of other simple and complex methods, but in the following example, the discount rate will be calculated for clarity and transparency of the main formula as the sum of the "risk-free rate" and the "risk premium". The first component of the equation - the risk-free rate - in the example of the calculation is equal to 15% - the key rate of the Central Bank of the Russian Federation. This is part of the return on the risk-free asset. The second component - the risk premium - is set by an expert method in the amount of 8% based on a conditional assessment of production, innovation, social, technological and other risks. This is the rate of return on existing risks. In total, the discount rate will be considered equal to 23%.

Calculation example

Our calculation example will correspond to the domestic tradition of choosing a forecasting period in the range of 3-5 years. Let's take an average of 4 years for a fictitious project with a discount rate of 23%.

- Let's write out for each year the projected amount of income in rubles (CI) and the amount of cash expense (CO). Here we choose an annual interval for analysis and will calculate the discounting of cash flows, first for each separate year, and then - the reduced flow in the sum for all 4 years. The projected consumption will be stable, and the income will vary from year to year.

- First year: + 95k and -30k

- Second year: + 47k and -30k

- Third year: + 54k and -30k

- Year 4: + 41k and -30k

- We calculate the difference between income and expenses for each year. It turns out that the sum of such differences for periods 1-4 will be 65, 17, 24 and 11 thousand rubles, respectively.

- We bring financial flows to the initial period. We use to calculate the coefficients 1 / (1 + 0.23) i that discount each stream. Here, in place of the dividend, there will be the difference between income and expenses for each year, which we calculated in the previous step. In place of the divisor, there is a coefficient, and the value of 0.23 is the discount rate of 23%, and the "i" to the power corresponds to the number of the year for which we are calculating.

- 65000/(1+0,23) = 52845

- 17000/(1+0,23) 2 = 11237

- 24000/(1+0,23) 3 = 12897

- 11000/(1+0,23) 4 = 4806

(* Results are written in rubles rounded to whole numbers).

- We add the received sums together, which gives DCF = 81,785 rubles.

Since the indicator ultimately has a positive value, we can talk about further analysis of the project's prospects. Investment analysis requires the use of a discounted cash flow method and a comparison of the totals for several alternative projects so that they can be ranked according to their attractiveness.

Basic methods such as ROCE and Payback can be used when evaluating capital projects. Alternatively, companies can use the DCF (Discounted Cash Flow) technique discussed on this page. With the help of the discounted cash flow technique, it is possible to calculate such popular indicators of investment performance as net present value (NPV) and internal rate of return (IRR).

Cash flows and relevant costs

For all investment valuation methods except ROCE, only the related cash flows should be considered. These:

- cash flows that will occur in the future;

- cash flows that will arise only in the event of an investment project or a capital investment project

An investment appraisal should always ignore:

- expenses incurred (expenses that have already been incurred)

- mandatory costs (costs that will be incurred in any case)

- non-cash expenses

- overheads.

Time value of money

Money received today is worth more than the same amount received in the future. This is a key principle in investment analysis called the time value of money.

This happens for three reasons:

- potential for interest / financing costs

- impact of inflation

- impact of risk.

Discounted cash flow (DCF) methods take this time value of money into account when evaluating investments.

Compounding

The amount invested today will bring interest. The compounding method calculates the future or final value of a given amount invested today in a few years.

To add up the amount, the key figure is increased by the amount of interest it earned over the period.

Compounding example:

An investment of $ 100 must be made today. What is the investment value in two years if the interest rate is 10%?

Solution

$ 100 will cost $ 121 over two years with a 10% interest rate.

Compounding Formula:

To speed up the computation of the blend, we can use a formula to calculate the future value of the amount nested now. Formula:

FV = PV * (1 + r) ^ n

where FV = future value after n periods

PV = Current or Initial Cost

r = interest rate for the period

n = number of periods

Discounting

In a potential investment project, cash flows will arise at different points in time. To make a useful comparison of the various flows, they all have to be converted to a common point in time, usually to date, ie, the cash flows are discounted.

Present value (PV) is the current cash equivalent of future receivables / payables.

Formula for discounting

PV = FV / (1 + r) ^ n

It is simply a reordering of the formula used for compounding.

(1 + r) -n is called the discount factor or discount factor (DF).

Discounting example:

What is PV of $ 115,000 due nine years later if r = 6%?

Solution:

Capital cost

In discounted cash flow methods, an interest rate is required. There are a number of alternative terms used to refer to the interest rate:

- cost of capital

- discount rate

- required return.

Various ways of determining the cost of capital are discussed here.

Net Present Value (NPV)

To estimate the overall project impact using DCF methods, discounting all relevant project-related cash flows to their present value (PV).

If we consider the project's outflow as negative and the inflow as positive, the NPV of the project is the sum of the present value (PV) of all flows arising from the project.

Decision rule:

NPV represents the surplus funds (after financing the investment) earned by the project, therefore:

- if NPV is positive - the project is financially viable

- if NPV is zero - the project breaks even

- if NPV is negative - the project is not financially viable

- if a company has two or more mutually exclusive projects, they should choose the one with the highest NPV

Assumptions in Calculating Net Present Value

In calculating the net present value, the following cash flow assumptions are made:

- all cash flows occur at the beginning or end of the year

- initial investment occurs T0

- other cash flows start one year after that (T1).

Also, interest payments are never included in the NPV calculation as they are accounted for at the cost of capital.

NPV usage example

The organization is considering an investment in new equipment. The estimated cash flows are as follows.

The company's cost of capital is 9%.

Calculate the NPV of a project to assess whether it should be run... Solution:

The PV of the cash inflow exceeds the PV of the cash outflow by $ 29,760, which means that the project will receive more than 9% DCF income, which means it will receive a surplus of $ 29,760 after the financing cost has been paid. Therefore, it should be carried out.

Advantages and Disadvantages of Using NPV

Advantages

In theory, the NPV investment appraisal method outperforms all others. This is because he:

- is an absolute measure of return

- based on cash flow, not profit

- should lead to maximization of shareholder wealth.

disadvantages

- Difficult to explain to managers

- Knowledge of the cost of capital is required

- It is relatively difficult.

Calculation of discount factors

However, in some special cases, time saving methods can be used.

Discount annuities

An annuity is a constant annual cash flow over a number of years.

If the investment valuation assumes a constant annual cash flow, a special discount rate known as the annuity rate can be used.

The annuity factor (AF) is the name assigned to the amount of an individual DF. Formula for the annuity rate:

An example of using the annuity coefficient:

The $ 3,600 fee is due every year for seven years, with the first payment due one year later. The interest rate is 8%. What is PV annuity.

Solution:

AF can be found by the formula:

Therefore, the PV of the annuity is $ 3600 x 5.206 = $ 18.741.60

Discounted perpetual payments (perpetuity)

Perpetual is an endless annual cash flow.

The present value (PV) of infinite cash flow is determined by the formula:

where, CF is the cash flow, r is the discount rate.

1 / r is also known as the coefficient or factor of eternity.

An example of using the eternity coefficient:

What is the current value of $ 3,000 received each year if the interest rate is 10%?

Solution:

Advanced and deferred annuities, perpetual payments, perpetuities

Using annuity factors and infinity factors assumes that the first cash flow will occur in a year. Thus, annuity or perpetuity ratios will reduce cash flows to give value one year before the first cash flow appears. For standard annuities and maturities, this gives the current value (T0) since the first cash flow starts at T1.

Be careful, if this is not the case, you will need to adjust your calculations.

In some investment valuations, regular cash flows may start now (at T0) rather than a year later (T1).

Calculate PV by ignoring the payment at T0 when considering the amount of cash flows, and then adding it to the annuity or eternity rate.

An example of using extended annuities

A 5-year annuity of $ 600 starts today. Interest rates are 10%. Find the PV of the annuity.

Solution

This is essentially a standard four-year annuity with an additional T0 payment. PV can be calculated as follows:

PV = 600 + 600 × 3.17 = 600 + 1902 = $ 2.502

The same answer can be found faster by adding 1 to AF:

PV = 600 x (1 + 3.17) = 600 x 4.17 = 2.502.

An example of using advanced perpetuities

The $ 2,000 perpetuity should start immediately. The interest rate is 9%. What is PV?

Solution

This is essentially a standard perpetual with an additional T0 charge. PV can be calculated as follows:

Again, the same answer can be found faster by adding 1 to eternity.

Deferred annuities and perpetuities

Some regular cash flows may start later than T1.

This applies to:

- applying an appropriate factor to cash flow as usual

- returning your answer back to T0.

Example of deferred annuities

For deferred cash flows, applying the standard annuity ratio will determine the value of the cash flows in the year before they start, which in this illustration stands for T2. To find PV, additional calculation is required, the value must be fed back to T0.

What is PV of $ 200 each year for four years starting from three years if the discount rate is 5%?

Solution

Internal Rate of Return (IRR)

IRR is another project assessment method using DCF methods.

IRR is the discount rate at which the NPV of an investment is zero. Thus, it represents the break-even cost of capital.

Calculating IRR using linear interpolation

Steps in linear interpolation:

- Calculate two NPVs for a project at two different capital costs

- Use the following formula to find the IRR:

L = lower interest rate

H = higher interest rate

NL = NPV at a lower interest rate

NH = NPV at a higher interest rate.

The chart below shows the IRR estimated by the formula.

Decision rule:

- projects must be accepted if their IRR is greater than the cost of capital.

An example of using IRR

The projected cash flows of the potential project yield an NPV of US $ 50,000 at a discount rate of 10% and an NPV of US $ 10,000 at a discount rate of 15%.

Calculate IRR.

Solution:

Advantages and disadvantages of IRR

Advantages

IRR has a number of advantages, for example. It:

- takes into account the time value of money

- is percentage and therefore easy to understand

- uses cash flows without profit

- considers the whole life of the project

- means that the firm selects projects in which the IRR exceeds the cost of capital, should increase the wealth of shareholders.

disadvantages

- This is not an absolute rate of return.

- Interpolation is only an estimate, and an accurate estimate requires the use of a spreadsheet program.

- It is rather difficult to calculate.

- Unconventional cash flows can lead to multiple IRRs, which means that the interpolation method cannot be used.

Difficulties with the IRR approach

Interpolation only gives an estimate (and an accurate estimate requires the use of a spreadsheet program). The cost of calculating capital itself is also only a rough estimate, and if the difference between the required return and the IRR is small, then this lack of accuracy could in fact mean that the wrong decision is being made.

Another disadvantage of IRRs is that unconventional cash flows can result in no IRR or multiple IRRs. For example, a project with an outflow in T0 and T2, but income in T1, may, depending on the size of cash flows, have several different profiles on different charts (see below). Even where the project has one IRR, the graph shows that the acceptance rule will lead to the wrong result, since the project does not receive a positive NPV at any cost for capital.

NPV vs IRR

Both NPV and IRR are investment valuation techniques that discounted cash flows and outperform basic techniques such as ROCE or ROI. However, only NPV can be used to distinguish between two mutually exclusive projects, as the diagram below demonstrates:

The profile of project A is such that it has a lower IRR and the application of the IRR rule would prefer project B. However, in absolute terms, A has a higher NPV in terms of the company's cost of capital and should therefore be preferred.

Thus, NPV is better suited for choosing between projects.

The advantage of NPV is that it speaks of an absolute increase in the wealth of shareholders as a result of the adoption of the project at the current cost of capital. The IRR simply tells us how much the cost of capital can rise before the project is not worth adopting.

Modified Internal Rate of Return (MIRR) addresses many of these issues with a regular IRR

Also on the topic investment appraisal

- Capital quotes

- Investment appraisal. Other aspects

The discounted cash flow method (DCF) is used to calculate the discounted price of cash flows from real estate properties.

Application of DDP

The DCF method allows you to evaluate any business, even if the incoming cash flows are unstable. In practice, it is used when:

- there is a sufficient amount of information data, the use of which makes it possible to determine the amount of future profit;

- there is a theory that future investments will be radically different from current ones;

- the object is a commercial property with a large area;

- there are differences between costs and profitable flows;

- the real estate object has just been put into operation or has not yet been built at all.

The main advantage of the DDP method is its versatility. An expert can easily calculate the size of future investments and determine the most qualitative paths for the development of an enterprise.

DCF calculation

The calculation of the DCF is carried out in several stages.

Determination of the forecast time period

The amount of information data that will be received by an expert to determine changes in financial flows depends on the accuracy of the forecast.

Profit forecasting

At this important stage, the researcher is required to:

- conduct a qualitative analysis of the volume of profits and costs over the past years;

- analyze and assess the situation on the real estate market;

- carry out a qualitative forecast of the distribution of future costs based on information data on past costs and income;

Assessment of an object using the DCF method is carried out taking into account all types of profit received by the company. It also calculates those financial flows that came before taxes and those that appeared later.

General Reverse Value Determination

Produced with:

- high-quality professional accounting of changes that occurred in the price of an object during the period that it was owned and operated in order to obtain financial benefits;

- set value of sales;

- capitalization of profits for a separately selected period.

Calculating the discount rate

It is used in the case when it is necessary to urgently calculate the cost of a financial flow, the receipt or payment of which is possible after a specific time period. An efficient and most reliable bet calculation is carried out using several effective methods:

- attachment comparison method. It is considered very effective in terms of calculating the investment price of the property selected for analysis;

- selection method. When calculating, the size of future income is necessarily taken into account and is compared with the initial investment.

- monitoring method. The situation on the real estate market is constantly monitored. All the data that were obtained in the course of observation are unified and presented for everyone to see. As a rule, such information acts for the evaluator as a kind of benchmark, based on which one can compare the average and current indicators.

Calculating the price of an object

The process of calculating the par value has several features, which must be taken into account without fail:

- firstly, in order to correctly calculate the reversal value, it is imperative to discount for the last year. After that, the reversion and the total amount of funds are summed up;

- secondly, at the end of the calculations, the value of the property selected for research should be equal to the total sum of two most important parameters - the reversion of the current type and the value of those cash flows that are planned to be received in the future.

Compliance with the above two conditions is mandatory, since otherwise the result will have large errors. It is only necessary to entrust the performance of all calculations to specially trained specialists.

Decide on the discount rate to use. It can be determined using the capital asset pricing model (CAPM) formula: risk-free rate of return + asset sensitivity to changes in market returns * (risk premium for investments with medium risk). For stocks, the risk premium is around 5%. Since the stock market values most stocks over a 10-year period, the risk-free rate of return on them will be equal to the yield on a 10-year Treasury bond. For the purposes of this article, let's say it is 2%. So, with a sensitivity of 0.86 (which means 86% exposure to market fluctuations for investments with an average risk in the general market), the discount rate for stocks will be 2% + 0.86 * (5%) = 6.3%.

Determine the type of cash flows to discount.

- Simple cash flow- This is a single receipt of funds in the future, for example, receiving $ 1000 in ten years.

- Annuity Cash flows are continuous cash receipts at fixed intervals over a specified period, such as receiving $ 1,000 annually over 10 years.

- Growing annuity cash flows are expected to grow at a constant rate over a period of time. For example, over 10 years, an amount of $ 1,000 will be received, increasing every year by 3%.

- Perpetuities(perpetual annuities) - Continuous, non-expiring cash inflows at regular intervals, such as a $ 1,000 annual preference dividend.

- Growing perpetuities- These are constant non-ending cash inflows at regular intervals, which are expected to grow at a constant rate. For example, a $ 2.2 stock dividend for the current year, followed by an annual increase of 4%.

To calculate discounted cash flow, use the appropriate formula:

- For simple cash flow: present value = future cash receipts / (1 + discount rate) ^ time period. For example, the present value of $ 1,000 in 10 years at a discount rate of 6.3% would be $ 1,000 / (1 + 0.065) ^ 10 = $ 532.73.

- For annuities: present value = annual cash flows * (1-1 / (1 + discount rate) ^ number of periods) / discount rate. For example, the present value of $ 1,000 received annually over 10 years at a discount rate of 6.3% would be $ 1,000 * (1-1 / (1 + 0.063) ^ 10) / 0.063 = $ 7256.60.

- For growing annuities: present value = cash flow * (1 + g) * (1- (1 + g) ^ n / (1 + r) ^ n) / (rg), where r = discount rate, g = cash flow growth factor, n = number of periods. For example, the present value of flows of $ 1000 with an annual increase of 3% over 10 years at a discount rate of 6.3% would be $ 1000 * (1 + 0.03) * (1- (1 + 0.03) ^ 10 / ( 1 + 0.063) ^ 10) / (0.063-0.03) = $ 8442.13.

- For perpetuities: present value = cash flows / discount rate. For example, the present value of the $ 1,000 regular dividend on preferred shares at a discount rate of 6.3% would be $ 1,000 / 0.063 = $ 15,873.02.

- For growing perpetuities: present value = expected next year cash flow / (discount rate - expected growth rate). For example, the present value of a $ 2.2 share dividend, which is expected to rise 4% next year, at a discount rate of 6.3% would be $ 2.20 * (1.04) / (0.063-0, 04) = $ 99.48.

Related Articles