Criteria for evaluating the work of metrologists. Economic standardization efficiency. Features of the formation of the economic effect, taking into account the error of measurements

All-Russian Research Institute

Metrological service

(VNIIMS)

State Standard of Russia

STATE SYSTEM FOR ENSURING UNIFORMITY OF MEASUREMENTS

Methods for determining the economic efficiency of metrological works

Mi 2546-99

Designed VNIIMS.

EXECUTOR Kulik K.V.

Inspend Mi 2447-98

This Recommendation establishes a system of indicators and methods for determining the economic efficiency of metrological work. The recommendation complies with the methodological guidelines for assessing investment projects and their selection on financing approved by the Russian State Building, the Ministry of Economy of the Russian Federation, the Ministry of Finance of the Russian Federation, the State Committee of Russia of March 31, 1991 No. 7-12 / 47.

1. General Provisions

Economic substantiation of programs and plans to improve the metrological support of production;

Decisions on the feasibility of conducting work on metrological support, including them into a plan, as well as for analyzing technical solutions for the purpose of choosing the best;

Estimates of the effectiveness of metrological services;

Developments in enterprises, organizations and sectors of methodological documents that take into account the specifics of assessing the effectiveness of metrological works associated with specific types of measurements and solved objectives for metrological support.

Creation and implementation of state standards;

Creating and implementing working standards;

Creating and implementing measurement tests;

Creation and introduction of standard samples of the composition and properties of substances and materials;

The introduction of the system of state tests of measuring instruments,

Creation and implementation of methods for calibration of measuring instruments;

Organization of verification and repair of measuring instruments;

Creating and implementing measurement methods;

Certification of measurement methods;

Development, scientific and technical expertise and the introduction of regulatory documentation regulating the implementation of metrological works;

Conducting metrological examination of technical documentation;

Conducting state metrological oversight and control;

Obtaining and applying standard reference data on physical constants and properties of substances and materials;

Development and implementation of automated information and management systems of metrological services.

1.3. The decision on the feasibility of working on metrological support is made by enterprises independently, taking into account data on the effectiveness of these works, determined by the planned or fixed period of time.

The expediency of the same approach to estimates of various variants of metrological support and social sphere;

Independence of economic entities in solving issues on the modernization of metrological support;

The desire for the maximum possible elimination of the influence of inaccuracies and incompleteness of information on the quality of the evaluation of the effectiveness of various options for the choice and the actual state of work on metrological support.

1.5. To assess the effectiveness of work on metrological support in accordance with apply the following indicators:

Commercial (financial) efficiency - determines the financial implications for direct participants (investors) of projects;

Budgetary efficiency - reflects the financial implications of the project for the federal, regional and local budget;

Economic efficiency - takes into account the costs and results that go beyond the direct financial interests of investors.

1.6. The introduction of new metrological developments in most cases is associated with the need to implement certain one-time costs, i.e. with investments. Therefore, the definition of the effectiveness of these developments is subject to the general rules for calculating the effectiveness of investment, the most important of which:

Development of a system of indicators and criteria for efficiency;

Definition of investment purposes;

Conducting calculations according to the procedures accepted, indicators and criteria;

Studying the reality of obtaining funds for the necessary investment, the size of which is determined as a result of the calculations;

Making decisions.

2. Indicators of commercial and economic efficiency

2.1. Commercial effectiveness of introducing new measuring instruments and other metrological developments is determined by the ratio of financial costs and results that ensure the required rate of profitability.

2.2. Pure discounted income of the CDD (integral effect e) is the excess of integral results over the integral costs shown to one time.

(2.1)

|

where - |

financial results achieved at the T-M period; |

|

current costs carried out on the same period; |

|

|

T - |

time period of calculation; |

|

calculation steps number; |

|

|

coefficient of discounting (solid) of high cost and results to one moment; |

|

|

the amount of discounted capital investments. |

In cases where, as a result of the development of development (project), the volume of products or services (in value terms) is applied (). If the volume of production does not change, but only costs change, acquires the form:

![]() (2.2)

(2.2)

|

where s 1 and z 2 - |

current costs of replaceable and new variant; |

|

the coefficient of bringing (discounting) of the rapid costs to one point. This coefficient reflects the cost of money in time and is determined by the formula |

(2.3)

If the formula is used for the case when the discount rate varies in time, the discount rate is equal

(2.4)

(2.4)

|

where - |

the rate of discount in the K is the year; |

|

accountable time period, year. |

, (2.5)

2.4. The internal rate of profitability (GNI) defines the calculation rate of the discount E, in which the value of the reduced effect is equal to the present costs (investments) and is determined from equality

![]() (2.6)

(2.6)

In the introduction of a large metrological project associated with many participants in the development and implemented for a number of years;

When introducing (upgrading) expensive measurement tools at the payback of one-time costs in a period exceeding one year.

2.5. Payback is called the time of development (project) until the time until the funds spent on investment be returned. This indicator gives the most accurate results when evaluating short-term projects with payback of capital investments in a period not exceeding one year. The payback period () in this case is determined by formulas

![]() (2.7)

(2.7)

or

![]() (2.8)

(2.8)

If capital investments are carried out for a number of years, payback period is calculated taking into account the discounting:

(2.9)

(2.9)

or

(2.10)

(2.10)

If the investment is carried out within one year, but it does not pay off for the year, then the number of years for which the integral effect (taking into account the discount) will reach or exceed the value of the capital investment.

Payback period is measured in months (if this indicator does not exceed one year) or in years.

2.6. None of the above indicators and criteria is not sufficient to fully assess the effectiveness of the project. Analysis must be subjected to a number of indicators. When making a decision on the implementation of the project, these indicators should be monitored.

2.7. In fairly simple cases, it is possible to limit ourselves to the analysis of the indicators of the integral effect, the index of profitability and in some cases of payback period.

2.8. The integral efficacy of metrological works, as well as any other types of work, reflects the aggregate savings of living labor, raw materials, materials, capital investments and additional income from more complete satisfaction of the needs of the national economy in ensuring the unity and required measurement accuracy.

2.9. Assessment of costs and results in the introduction of new metrological developments is carried out within the estimated period. The duration of the latter (calculation horizon) is determined with the time required for implementation, and the regulatory life of new measuring instruments. The cost of holding metrological works includes the current and one-time costs of all participants in the implementation of activities, calculated without a re-account of the same costs, and without taking into account the costs of some participants in the results of other participants.

2.9.1. The one-time capital expenditures for the implementation of the projects, as a rule, include the costs associated with the following work:

Construction (reconstruction) of laboratory premises;

Acquisition (rent) of the appropriate equipment;

R & D associated with the development of new equipment;

NIR related to the development of regulatory documentation;

Accreditation and / or / licensing of laboratories for the right to perform relevant types of work (testing, certification, calibration, calibration, repair of measuring instruments);

Tests and certification of equipment that has not passed this procedure earlier;

Preparation, retraining, personnel certification.

2.9.2. To current costs include:

Expenses for the purchase of raw materials, materials, purchased semi-finished products;

Operating costs for the maintenance of premises and equipment and / or / rent;

Staff keeping costs;

Travel and transportation costs.

Note: The operational expenses do not include depreciation deductions for the fixed assets that were acquired at the expense of funds taken into account in one-time costs.

2.10. When evaluating the costs and economic results of project implementation, basic, world, forecast and estimated prices for goods and services used can be used.

2.10.1. Base prices - prices established at a certain point in time. They are used, as a rule, at the stage of technical and economic research the possibility of implementing the project.

2.10.2. Fortex prices - prices at the end of the T-th period of the program implementation (project) in accordance with the projected price change index for goods and services.

They are determined by the formula:

(2.11)

|

where - |

the forecast price for the end of the T-th period of the program implementation (project); |

|

basic price of goods or services; |

|

|

the index of changing the price of the relevant product or service at the end of the T-th period of the program implementation (project) in relation to the moment of adoption of the basic price. |

2.10.3. Estimated prices - prices calculated similarly to the forecast prices, but a common inflation index (deflator) is used as a price change index.

2.10.4. World prices - prices for goods and services corresponding to the prices of the world market and expressed in a sustainable world currency (US dollars, German brands, ecu, euro, etc.). World prices may also be basic, calculated and forecast.

2.10.5. According to metrological measures of federal targeted programs and other programs and projects developed by order of federal executive bodies, the values \u200b\u200bof price change indices for certain types of products and resources should be established in the task of developing or designing objects in accordance with the forecasts of the Ministry of Economy of Russia.

2.10.6. The objectives of the events may be to solve individual private tasks (labor protection at the enterprise, the ecology of the region, the solution of aesthetic problems with the impossibility of changing prices for products, an increase in jobs, etc.). Calculated in these cases, indicators of commercial or economic efficiency are reference in nature, since their negative significance does not mean a mandatory refusal of the event.

2.11. If the implementation of the event to improve the metrological provision of production is associated with large one-time costs or significantly reflects on the economic indicators of the enterprise (implementation participants), the flow and balance of real money should also be calculated.

2.11.1. When implementing projects, there are three types of activities: investment, operational and financial. Within each type of activity, the influx and cash outflow occurs. The flow of real money is the difference between the influx and outflow of funds from investment and operating activities.

The balance of real money is called the difference between the influx and outflow of funds from all three activities.

2.11.2. Detailed instructions on the calculation of the flow and the balance of real money are contained in section 3.

2.12. The formula () of determining the integral economic effect for sufficiently simple cases can be transformed into a simpler expression.

At the same time, the formula takes the form

![]() (2.12)

(2.12)

|

where a - |

annual production; |

|

C 1 and C 2 - |

cost of old and new options. |

or

![]() (2.13)

(2.13)

2.13. In the event that the results of technical and commercial analysis do not allow us to conclude the possibility of commercial use of the results achieved in the implementation of the project, all costs associated with the implementation of these activities are additional costs, therefore it is necessary to carry out costs.

In this case, the estimate of the economic effect is based on comparison of costs for various embodiments of the project. Effective consider an option that provides a minimum of the costs:

![]() (2.14)

(2.14)

3. Budget efficiency

3.1. Budgetary efficiency indicators reflect the impact of the results of the event on the revenues of the relevant (federal, regional and local) budgets.

3.2. The main indicator of budget efficiency is the budget effect.

3.3. The budget effect is calculated on all major developments aimed at improving the metrological provision of production, the creation of which the budget of any level takes part. The budget effect is also calculated on those projects, the implementation of which is associated with a significant increase in the receipt of funds to the budget.

3.4. Methods for calculating budgetary efficiency are similar to previously shown, but taking into account the current tax legislation.

4. Features of the formation of an economic effect, taking into account the measurement error

4.1. The main source of effect formation is to reduce losses in the economic system, provided by the creation of legal, regulatory, organizational, technical and economic conditions necessary to solve problems for obtaining measuring information with certain accuracy and reliability, as well as adoption on this measuring information of solutions.

4.2. The economic effect (E) is determined from the following expression:

![]() (4.1)

(4.1)

4.3. Losses from measurement errors in general include the following components:

![]() (4.2)

(4.2)

|

where - |

losses from the fictitious marriage of standards on metrological characteristics; |

|

losses due to the fictitious marriage of measurement tools for metrological characteristics; |

|

|

losses arising in the economic system from the error of the workshop of measurements or the use of measurement methods that do not provide the required accuracy and accuracy. |

4.3.1. Depending on the task, to solve the measuring information, the loss of measurement error in the economic system are classified as follows:

Losses from measurement errors in measuring control of equipment parameters, input control and product quality control;

Losses arising from measurement errors in flow operations, accounting, dosing, which is extremely important when working with expensive material;

Losses arising from the deviation of the technological process parameters from optimal values \u200b\u200bdue to measurement errors.

4.3.2. The savings received from the reduction of measurement errors in measuring control of equipment parameters, input control and product quality control can occur due to:

Reduce losses from missing defective measurement tools and subsequent operation;

Reduce non-production costs when passing defective products, materials, semi-finished products and rejection of suitable controls;

Reduction of losses from rejection of waste products during the output control, as well as from fines and complaints due to the passage of defective products in the consumption sector;

Reduce costs when skipping defective parts and nodes into the production cycle;

Reduction of damage from the operation of defective products from the consumer;

Improve the quality of products and reduce the consumption of materials during the certification of technological equipment for accuracy;

Reduction of equipment downtime and loss from accidents and breakdowns;

Reducing losses from reducing the quality of products, etc.

4.3.3. With flow measurement, accounting, dosing increase in measurement accuracy can lead to a decrease:

Regulatory losses upon leave for materials, raw materials, semi-finished products, energy and finished products;

The amount of penalties for incomprehensible material resources;

Overpowering material resources;

Loss from improper accounting of material resources;

Losses from deterioration of quality and reduce the variety of products, etc.

4.3.4. When controlling technological processes, the increase in measurement accuracy can lead to a decrease:

Consumption of material resources when approaching the measured parameters of the processes to optimal values;

Loss from breakdowns, equipment accidents and reduce its service life.

4.3.5. The determination of losses from measurement errors is carried out by experimental or calculated methods, taking into account the type and parameters of the distribution laws of the measured (controlled) parameter and measurement errors for specific organizational and technical conditions.

4.3.6. When carrying out accounting and settlement operations using appropriate measurement tools, a conditional economic indicator with P - "cost of error" can be used, reflecting the economic risk of "Seller" and "Buyer":

Under the metrological support (MO) of measurements is meant "The activities of metrological and other services, aimed at: Creation of the necessary standards, exemplary and working tools in the country; the right choice and application;, development and application of metrological rules and norms; The implementation of other metrological works required to ensure the required quality of measurements in the workplace, the enterprise (organization), in the Ministry (Office), the People's Economy.

As the definition of this term shows, the concept of self is wide enough - from the organization of technical measurements to ensuring the unity of measurements and legislative metrology.

For industrial enterprises, developers and users of measuring instruments, practical interest is part of the MO associated with the activities of the metrological service (MS) of the enterprise. In this regard, the terms "Metrological support of the enterprise", "Metrological provision of production" (MOP) received widespread.

MOS, mostly includes:

Analysis of measurement status;

Establishing a rational nomenclature of measured values \u200b\u200band use of measuring instruments (workers and reference) appropriate accuracy;

Carrying out the calibration and calibration of measuring instruments;

Development of measurement methods for ensuring established accuracy norms;

Conducting metrological examination of design and technological documentation;

Introduction of the necessary regulatory documents (state, industry, branded);

Accreditation for technical competence;

Conducting metrological oversight.

In the conditions of market relations, when the main purpose of the enterprise is the profit used by measuring instruments, as part of fixed assets, should work on this main goal.

MOS should be able to optimize the management of technological processes and the enterprise as a whole, stabilize the processes, maintain the quality of product manufacturing. At the same time, the costs of MOP should correspond to the scale of production, the complexity of technological cycles and ultimately not only pay off, but also return profit. The assessment of the adequacy and economic efficiency of MOPs may provide serious organizational and methodological assistance to the recommendations of the MI 2240-92, developed by the All-Russian Research Institute of Metrological Service (VNII). Analysis of the status of measurements, control and testing at the enterprise, in the organization, association.

The document can be used in the development and certification of quality systems, with accreditation on technical competence, to develop programs for improving metrological support, etc. The document contains a "methodology for assessing the economic efficiency of measures to improve the state of measurements, control, testing, metrological support in the enterprise." Annex 2 "Informational support is very interesting and useful. Scenario of dialogue and algorithms for automated processing of information on measurement status analysis, control, enterprise testing. The addition of this material with the corresponding software product and technical means will allow you to automate the activities of the metrological service of the enterprise and reduce the amount of routine operations, facilitates the calculation of the economic efficiency of the MOS and will increase its effectiveness. Extremely tempting is modeling MOP options with various parameters and the subsequent calculation of their economic efficiency;

scanning options can provide an automatic search (selection) of the optimal MOP.

These recommendations and their use in the enterprise in some cases are necessary, under certain circumstances - useful, and the professional development of the analysis methodology with modern technical equipment may become an additional type of activity that makes considerable income.

9.1. The main terms in the field of metrology. Dictionary-Directory, M., Publishing House of Standards. 1989.

9.2. Reich N.N. , Tupichenkov A.A., Zeitlin V.G., Metrological provision of production. M., Publishing House. 1987.

METROGOLOGICAL EFFICIENCY The concept of effectiveness is applied in many sciences, including in metrology, as a characteristic of the quality of targeted metrological activity of a person and its results at different levels of knowledge of the essence of properties, processes, measuring instruments and measuring systems.

METROGOLOGICAL EFFICIENCY The concept of effectiveness is applied in many sciences, including in metrology, as a characteristic of the quality of targeted metrological activity of a person and its results at different levels of knowledge of the essence of properties, processes, measuring instruments and measuring systems.

Definition of MO - approval and application of metrological norms, rules and measurement methods also develop, manufacture and applying technical means to ensure unity and required measurement accuracy.

Definition of MO - approval and application of metrological norms, rules and measurement methods also develop, manufacture and applying technical means to ensure unity and required measurement accuracy.

Information on the amount and quality of manufactured products is obtained as a result of measurements. Depending on the complexity of products, its quality, the share of measurement costs varies in the large range. Thus, in the production of integrated circuits, these costs are 25 -50%, and radio facilities - 2025%, buses - 10%, in the confectionery, shoe, textile industry - 2 -4%. Measurement quality depends on the quality of measuring instruments used methods of measurement, frame qualifications, quality of operation and maintenance of measuring instruments.

Information on the amount and quality of manufactured products is obtained as a result of measurements. Depending on the complexity of products, its quality, the share of measurement costs varies in the large range. Thus, in the production of integrated circuits, these costs are 25 -50%, and radio facilities - 2025%, buses - 10%, in the confectionery, shoe, textile industry - 2 -4%. Measurement quality depends on the quality of measuring instruments used methods of measurement, frame qualifications, quality of operation and maintenance of measuring instruments.

Measuring Process Quality Measuring Means Measurement Measurement Result Environment Option Parameter Measurement Measurement Operator Input Product Standard Measuring Process - Process that converts the value of the measured parameter to the measurement result by using resources (measuring equipment and other equipment, the operator, the environment, etc. ), regulated by the measurement method. Measuring process model

Measuring Process Quality Measuring Means Measurement Measurement Result Environment Option Parameter Measurement Measurement Operator Input Product Standard Measuring Process - Process that converts the value of the measured parameter to the measurement result by using resources (measuring equipment and other equipment, the operator, the environment, etc. ), regulated by the measurement method. Measuring process model

Indicators of the quality of the measuring process The quality of the measuring process The accuracy of measurements is the correct measurement results of the measurement validity of measurements precision measurement results of the measurement results

Indicators of the quality of the measuring process The quality of the measuring process The accuracy of measurements is the correct measurement results of the measurement validity of measurements precision measurement results of the measurement results

Measurement accuracy is the measurement quality indicator that reflects the proximity of their results to the true value of the measured value; To describe the measurement accuracy in GOST R ISO 5725. 1 - 2002 "The accuracy (correctness and precision) of methods and measurement results" uses two terms: correctness and precision. Measurement error is the deviation of the measurement result from the true value of the measured value; The correctness of measurements is the measurement quality indicator, characterizes the degree of proximity of the average arithmetic value of a large number of measurement results to the true value and is estimated by the displacement of the mean arithmetic value at repeated FV measurements from the true value. .

Measurement accuracy is the measurement quality indicator that reflects the proximity of their results to the true value of the measured value; To describe the measurement accuracy in GOST R ISO 5725. 1 - 2002 "The accuracy (correctness and precision) of methods and measurement results" uses two terms: correctness and precision. Measurement error is the deviation of the measurement result from the true value of the measured value; The correctness of measurements is the measurement quality indicator, characterizes the degree of proximity of the average arithmetic value of a large number of measurement results to the true value and is estimated by the displacement of the mean arithmetic value at repeated FV measurements from the true value. .

Ensuring unity of measurements Unity of measurements - such a state of measurements in which their results are expressed in legalized units, the dimensions of which correspond to units reproduced by the references, and the errors of measurement results do not go out for the established limits. That is, the unity of measurements ensures comparability of measurement results performed at different times, in various places, different means and methods.

Ensuring unity of measurements Unity of measurements - such a state of measurements in which their results are expressed in legalized units, the dimensions of which correspond to units reproduced by the references, and the errors of measurement results do not go out for the established limits. That is, the unity of measurements ensures comparability of measurement results performed at different times, in various places, different means and methods.

Ensuring the unity of measurements The convergence of measurements is their quality indicator, reflecting the proximity to each other, the measurement results performed at the same conditions of the same measured value. Reproducibility of measurements - their quality indicator, reflecting the proximity to each other, measurement results (one and the same measured value) performed in various conditions (at different times, in various places, by different methods).

Ensuring the unity of measurements The convergence of measurements is their quality indicator, reflecting the proximity to each other, the measurement results performed at the same conditions of the same measured value. Reproducibility of measurements - their quality indicator, reflecting the proximity to each other, measurement results (one and the same measured value) performed in various conditions (at different times, in various places, by different methods).

Inputs Measuring Process Algorithm Start Study of the Measuring Process to Stability Control Map Measuring Process No Process Stable? Eliminating special causes of variability of the measuring process Yes Evaluation of the displacement of the measuring process Evaluation of convergence (C) and reproducibility (c) Measurement results are not C and in acceptable? Constructive technological documentation Protocols for analyzing measurement process Yes Analysis of the suitability of the measuring process. End outputs Reduction of the influence of conventional causes of variability of the measuring process, additional research Protocol for analyzing the measuring process. Evaluation of the displacement and linearity. Scheme of estimation of the statistical characteristics of the measuring process

Inputs Measuring Process Algorithm Start Study of the Measuring Process to Stability Control Map Measuring Process No Process Stable? Eliminating special causes of variability of the measuring process Yes Evaluation of the displacement of the measuring process Evaluation of convergence (C) and reproducibility (c) Measurement results are not C and in acceptable? Constructive technological documentation Protocols for analyzing measurement process Yes Analysis of the suitability of the measuring process. End outputs Reduction of the influence of conventional causes of variability of the measuring process, additional research Protocol for analyzing the measuring process. Evaluation of the displacement and linearity. Scheme of estimation of the statistical characteristics of the measuring process

Properties and indicators of reliability of measuring instruments Reliability of measuring instruments Indicators Comprehensive properties Understanding Middle Establishment to failure Durability Middle Resource Maintainability Average Recovery Time Saveability Middle Deadlies Detection Care Protection Single

Properties and indicators of reliability of measuring instruments Reliability of measuring instruments Indicators Comprehensive properties Understanding Middle Establishment to failure Durability Middle Resource Maintainability Average Recovery Time Saveability Middle Deadlies Detection Care Protection Single

Undetyability is a measurement properties to continuously maintain a working condition for some time. It is characterized by two states: workable and inoperable. Durability is a property of the measurement tool to maintain a working condition before the marginal state when the maintenance and repair system is installed. Maintainability is a property of the measurement tool, which consists in the adaptability of the measurement tools to the prevention and detection of the causes of failures and maintenance and (or) restoration of a working state by carrying out maintenance and repair. Saveability - Properties Measurement Means Save the values \u200b\u200bof measurement indicators, durability and maintainability during and after storage and transportation.

Undetyability is a measurement properties to continuously maintain a working condition for some time. It is characterized by two states: workable and inoperable. Durability is a property of the measurement tool to maintain a working condition before the marginal state when the maintenance and repair system is installed. Maintainability is a property of the measurement tool, which consists in the adaptability of the measurement tools to the prevention and detection of the causes of failures and maintenance and (or) restoration of a working state by carrying out maintenance and repair. Saveability - Properties Measurement Means Save the values \u200b\u200bof measurement indicators, durability and maintainability during and after storage and transportation.

XIX century § Appearance of accurate devices, § Development of the measurement system Today expansion of the nomenclature, n number of measurements of N and the increase in their accuracy N

XIX century § Appearance of accurate devices, § Development of the measurement system Today expansion of the nomenclature, n number of measurements of N and the increase in their accuracy N

The oscillation of measurements is an important condition for the development of international cooperation and trade. In 1875, the metric convention was signed in 1875 (the manufacture of international and national prototypes of meters and a kilogram, the creation of metrological institutions was envisaged)

The oscillation of measurements is an important condition for the development of international cooperation and trade. In 1875, the metric convention was signed in 1875 (the manufacture of international and national prototypes of meters and a kilogram, the creation of metrological institutions was envisaged)

Uniformity of measuring instruments up to 70s, the focus of specialists in the field of metrology was focused on providing uniformity of measurement tools. In the late 60s in Russia, the transition from the uniformity of measurements to ensure the unity of measurements - GSI ensuring the unity of measurements (the results are pronounced in the legalized unity and measurement errors are known with a given probability)

Uniformity of measuring instruments up to 70s, the focus of specialists in the field of metrology was focused on providing uniformity of measurement tools. In the late 60s in Russia, the transition from the uniformity of measurements to ensure the unity of measurements - GSI ensuring the unity of measurements (the results are pronounced in the legalized unity and measurement errors are known with a given probability)

GOST 16263 -70 "State system for ensuring unity of measurements. METROLOGY. Terms and definitions "Only the technical aspect of metrological activity - the cost of unity of measurements in 1976 was approved by GOST 1. 25 -76 and the concept of" metrological support "of GOST 1. 25 -76" State standardization system was entered into the use of metrologists. Metrological provision. Basic Provisions »Technical + Economic Aspects of Metrological Activities - Measurement Unity + Accuracy Required

GOST 16263 -70 "State system for ensuring unity of measurements. METROLOGY. Terms and definitions "Only the technical aspect of metrological activity - the cost of unity of measurements in 1976 was approved by GOST 1. 25 -76 and the concept of" metrological support "of GOST 1. 25 -76" State standardization system was entered into the use of metrologists. Metrological provision. Basic Provisions »Technical + Economic Aspects of Metrological Activities - Measurement Unity + Accuracy Required

Features of MO Currently: Output control ("OF-LINE") - Messages are carried out between the relevant stages of processing parts or products transition to the control of the technological process and the management of them ("On-line"). Production parameters are measured directly during the process

Features of MO Currently: Output control ("OF-LINE") - Messages are carried out between the relevant stages of processing parts or products transition to the control of the technological process and the management of them ("On-line"). Production parameters are measured directly during the process

Requirements ISO 9001 to MS\u003e 7. 6 Control and measuring instruments\u003e Organization should establish control and measurements to be implemented, as well as define control and measuring devices necessary to ensure the certificate of product compliance with the established requirements.

Requirements ISO 9001 to MS\u003e 7. 6 Control and measuring instruments\u003e Organization should establish control and measurements to be implemented, as well as define control and measuring devices necessary to ensure the certificate of product compliance with the established requirements.

Scientific basis of unity; Principles; Methods; Errors; Metrological Metrological Support Measurement Metrological Support Maintenance Engineering Basics Legal Fundamentals Organizational Basics Creation and Use of SI; Selection and application of norms; Ensuring the quality of measurements of the Russian Law "On Ensuring the Unity of Measurements", regulations, regulatory acts The quality management system; Principles and documented ISO 9000 procedures; Processing approach Metrological service Analysis of efficiency use of the foundations of metrology Internal metrological control and supervision of the State Metrological Control and Supervision Audit

Scientific basis of unity; Principles; Methods; Errors; Metrological Metrological Support Measurement Metrological Support Maintenance Engineering Basics Legal Fundamentals Organizational Basics Creation and Use of SI; Selection and application of norms; Ensuring the quality of measurements of the Russian Law "On Ensuring the Unity of Measurements", regulations, regulatory acts The quality management system; Principles and documented ISO 9000 procedures; Processing approach Metrological service Analysis of efficiency use of the foundations of metrology Internal metrological control and supervision of the State Metrological Control and Supervision Audit

Monitoring and measurements on ISO 9001: 2011 \u003e\u003e\u003e\u003e 8. Measurement, analysis and improvement 8. 2. Monitoring and measurement 8. 2. 1. Consumer satisfaction 8. 2. 2. Internal audits (verification) 8. 2. 3. Monitoring and measurement of processes 8. 2. 4. Control and measurement of products 8. 3. Management of inappropriate products 8. 4. Data analysis 8. 5. Improvement 8. 5. 1. Continuous improvement 8. 5. 2. Corrective actions 8. 5. 3. Warning actions

Monitoring and measurements on ISO 9001: 2011 \u003e\u003e\u003e\u003e 8. Measurement, analysis and improvement 8. 2. Monitoring and measurement 8. 2. 1. Consumer satisfaction 8. 2. 2. Internal audits (verification) 8. 2. 3. Monitoring and measurement of processes 8. 2. 4. Control and measurement of products 8. 3. Management of inappropriate products 8. 4. Data analysis 8. 5. Improvement 8. 5. 1. Continuous improvement 8. 5. 2. Corrective actions 8. 5. 3. Warning actions

Monitoring and measuring on ISO 9001: 2011\u003e It is necessary to measure and monitor (in order to demonstrate the efficiency of the QMS processes):\u003e Consumer satisfaction (feedback information, market needs, competing, etc.); \u003e Achieving the goal as an audit output (accuracy of measurements and control, quality cost, resource efficiency, efficiency of processes, statistical control, information technology, motivation, including staff satisfaction); \u003e SMF processes to achieve planned results (their speed, accuracy, performance, reliability, etc.); \u003e Products (traditionally).

Monitoring and measuring on ISO 9001: 2011\u003e It is necessary to measure and monitor (in order to demonstrate the efficiency of the QMS processes):\u003e Consumer satisfaction (feedback information, market needs, competing, etc.); \u003e Achieving the goal as an audit output (accuracy of measurements and control, quality cost, resource efficiency, efficiency of processes, statistical control, information technology, motivation, including staff satisfaction); \u003e SMF processes to achieve planned results (their speed, accuracy, performance, reliability, etc.); \u003e Products (traditionally).

1) Metrological support is not a branch, but a type of activity (permeates the entire structure of social production); 2) the result of this activity is the measuring information for making management solutions (no products or services that can be assessed in monetary terms); 3) the structure of metrological support is hierarchychny (the transmission of the size of a physical size unit occurs along the steps of the test circuit from the standards of exemplary and working means of measurements); 4) Means of metrological support are meters of the main indicator of the country's development - national income.

1) Metrological support is not a branch, but a type of activity (permeates the entire structure of social production); 2) the result of this activity is the measuring information for making management solutions (no products or services that can be assessed in monetary terms); 3) the structure of metrological support is hierarchychny (the transmission of the size of a physical size unit occurs along the steps of the test circuit from the standards of exemplary and working means of measurements); 4) Means of metrological support are meters of the main indicator of the country's development - national income.

For active impact on the level of metrological support in industries, an analysis of the measurement status is carried out. Analysis objectives: -The establishment of compliance of MO to modern production requirements and the development of proposals for planning its further development; - the creation of methods and means of measuring and control required to intensify the production, creating and introducing new types of equipment and technologies, improving the quality of products, more rational use of resources; - Improving the reliability of measurement results when monitoring the state of the environment and monitoring the working conditions.

For active impact on the level of metrological support in industries, an analysis of the measurement status is carried out. Analysis objectives: -The establishment of compliance of MO to modern production requirements and the development of proposals for planning its further development; - the creation of methods and means of measuring and control required to intensify the production, creating and introducing new types of equipment and technologies, improving the quality of products, more rational use of resources; - Improving the reliability of measurement results when monitoring the state of the environment and monitoring the working conditions.

When analyzing the state of measurements, the influence of the state of the MO on the main technical economic indicators of production is revealed: - the quality, accounting system and production time; - labor productivity - economy of various types of resources and operating costs; - Reducing product costs.

When analyzing the state of measurements, the influence of the state of the MO on the main technical economic indicators of production is revealed: - the quality, accounting system and production time; - labor productivity - economy of various types of resources and operating costs; - Reducing product costs.

To study the impact of the level of production of production on technical and economic indicators, the following tasks can be distinguished: 1) find the optimal nomenclature of parameters and the optimal accuracy of their measurements (which parameters measure and with what accuracy); 2) determine the effectiveness of work on MO when driving to the optimum. so

To study the impact of the level of production of production on technical and economic indicators, the following tasks can be distinguished: 1) find the optimal nomenclature of parameters and the optimal accuracy of their measurements (which parameters measure and with what accuracy); 2) determine the effectiveness of work on MO when driving to the optimum. so

Therefore, it is necessary to develop methods for determining the economic efficiency of work on optimizing the nomenclature of parameters and accuracy of measurements. If the measuring information is used to control the technological processes, the measurement errors lead to deviations of the actual values \u200b\u200bof the modes on the specified nominal, which causes negative economic consequences.

Therefore, it is necessary to develop methods for determining the economic efficiency of work on optimizing the nomenclature of parameters and accuracy of measurements. If the measuring information is used to control the technological processes, the measurement errors lead to deviations of the actual values \u200b\u200bof the modes on the specified nominal, which causes negative economic consequences.

Economic efficiency of work on metrological support (MO) § Under the economic efficiency of metrological works is understood as the level of savings and extractable labor in public production, compulstent with the necessary costs. § Economic efficiency is assessed in order to choose the most promising areas for the development of the metrological service, a technical economic substantiation of plans for improving MO production, assessing the results of work for the reporting period and determining the technical and economic level of development of the metrological service.

Economic efficiency of work on metrological support (MO) § Under the economic efficiency of metrological works is understood as the level of savings and extractable labor in public production, compulstent with the necessary costs. § Economic efficiency is assessed in order to choose the most promising areas for the development of the metrological service, a technical economic substantiation of plans for improving MO production, assessing the results of work for the reporting period and determining the technical and economic level of development of the metrological service.

Principles of assessing the economic efficiency of work on MO: Ø Systematic approach to the analysis of the economic effect of work on metrological support; Ø metrological support covers the entire HCP; Ø Accounting time factor.

Principles of assessing the economic efficiency of work on MO: Ø Systematic approach to the analysis of the economic effect of work on metrological support; Ø metrological support covers the entire HCP; Ø Accounting time factor.

The economic effect of comparing two variants of measurement tools is determined by the formula: e \u003d (s 1 + p 1 nx) - (s 2 + p 2 nx)

The economic effect of comparing two variants of measurement tools is determined by the formula: e \u003d (s 1 + p 1 nx) - (s 2 + p 2 nx)

The main types of work on metrological support at enterprises: 1) ensuring the unity of measurements in the development, production and testing of products; 2) analysis and establishment of a rational nomenclature of measured parameters and optimal measurement accuracy norms when monitoring product quality indicators, technological processes, control of the characteristics of technological equipment; 3) organization and provision of metrological maintenance of measuring instruments: accounting, storage, calibration, calibration, alignment, adjustment, repair;

The main types of work on metrological support at enterprises: 1) ensuring the unity of measurements in the development, production and testing of products; 2) analysis and establishment of a rational nomenclature of measured parameters and optimal measurement accuracy norms when monitoring product quality indicators, technological processes, control of the characteristics of technological equipment; 3) organization and provision of metrological maintenance of measuring instruments: accounting, storage, calibration, calibration, alignment, adjustment, repair;

4) Development and implementation of measurement measurement techniques in the production process that guarantee the necessary measurement accuracy; 5) implementation of supervision of control, measuring and test equipment in real operating conditions, for compliance with the established metrological rules and norms; 6) conducting metrological examination of design and technological documentation; 7) organization and provision of metrological maintenance of test equipment: accounting, certification in accordance with the established requirements, repair;

4) Development and implementation of measurement measurement techniques in the production process that guarantee the necessary measurement accuracy; 5) implementation of supervision of control, measuring and test equipment in real operating conditions, for compliance with the established metrological rules and norms; 6) conducting metrological examination of design and technological documentation; 7) organization and provision of metrological maintenance of test equipment: accounting, certification in accordance with the established requirements, repair;

11) ensuring reliable accounting for the consumption of material, raw materials and fuel and energy resources; 12) introduction of modern methods and measuring instruments, automated control and measuring equipment, measuring systems; 13) evaluating the technical and economic consequences of the inaccuracy of measurements; 14) the development and implementation of regulatory documents regulating issues of metrological support; 15) Equaluation of economic efficiency.

11) ensuring reliable accounting for the consumption of material, raw materials and fuel and energy resources; 12) introduction of modern methods and measuring instruments, automated control and measuring equipment, measuring systems; 13) evaluating the technical and economic consequences of the inaccuracy of measurements; 14) the development and implementation of regulatory documents regulating issues of metrological support; 15) Equaluation of economic efficiency.

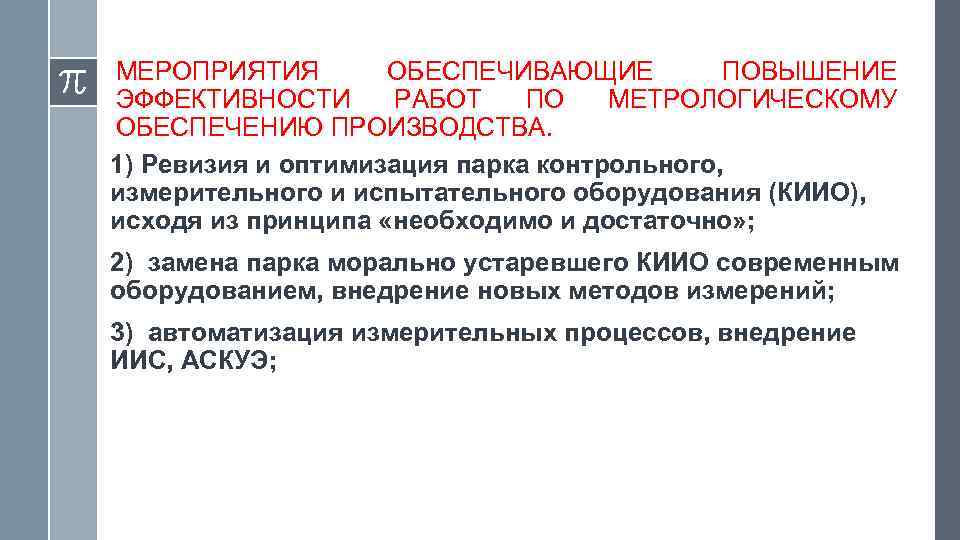

Events ensuring an increase in the efficiency of work on metrological provision of production. 1) revision and optimization of the control, measuring and test equipment fleet (KIIO), based on the principle "necessary and enough"; 2) replacement of the park morally obsolete kiyo with modern equipment, the introduction of new measurement methods; 3) automation of measuring processes, the introduction of IIS, AUSCE;

Events ensuring an increase in the efficiency of work on metrological provision of production. 1) revision and optimization of the control, measuring and test equipment fleet (KIIO), based on the principle "necessary and enough"; 2) replacement of the park morally obsolete kiyo with modern equipment, the introduction of new measurement methods; 3) automation of measuring processes, the introduction of IIS, AUSCE;

4) Optimization of measurement accuracy for economic criteria: - analysis of the importance of measuring information; - the use of more accurate si in responsible sites, the use of si with a coarse accuracy class, where it is advisable; - analysis of the calculation of the total measurement errors, the transition, where it is advisable, from arithmetic summation to the geometric; 5) improving the procedures of calibration, calibration, repair C (introduction of new standards, accreditation of metrological service, etc.), taking into account economic efficiency;

4) Optimization of measurement accuracy for economic criteria: - analysis of the importance of measuring information; - the use of more accurate si in responsible sites, the use of si with a coarse accuracy class, where it is advisable; - analysis of the calculation of the total measurement errors, the transition, where it is advisable, from arithmetic summation to the geometric; 5) improving the procedures of calibration, calibration, repair C (introduction of new standards, accreditation of metrological service, etc.), taking into account economic efficiency;

8) improving the professional level of personnel engaged in issues of metrological support; Intervals for increasing the metrological level of specialists of other departments (design, technological, industrial, testing) 9) streamlining the structure of the metrological support service. 10) Development of documents on metrological support of production (MOS) in accordance with GOST R ISO 9001 -2011. 14) Close interaction of the metrological service of the enterprise with regional CSM and metrological services of other organizations (enterprises).

8) improving the professional level of personnel engaged in issues of metrological support; Intervals for increasing the metrological level of specialists of other departments (design, technological, industrial, testing) 9) streamlining the structure of the metrological support service. 10) Development of documents on metrological support of production (MOS) in accordance with GOST R ISO 9001 -2011. 14) Close interaction of the metrological service of the enterprise with regional CSM and metrological services of other organizations (enterprises).

Improving the qualifications of metrologists: - development of work, methods of calibration and verification of new incoming measurement tools; - the study of the new law "On the provision of unity of measurements" and new regulatory documents on metrology; - training on retraining courses, various seminars conducted by the leading metrological institutions of the country (VNIIMS, VNIYM. D. I. Mendeleev); - participation in contests, metrology competitions; - study of periodicals by metrology - the active use of the electronic database equipped with a flexible information search system and automatically updated as new information appears: - On the technical characteristics of measuring instruments made to the State Register and approved; - about the calibration and repair work carried out by state metrological services of legal entities; - on regulatory and reference documents in the field of metrology; - on the standards and installations of the highest accuracy; - Electronic directories of outputs.

Improving the qualifications of metrologists: - development of work, methods of calibration and verification of new incoming measurement tools; - the study of the new law "On the provision of unity of measurements" and new regulatory documents on metrology; - training on retraining courses, various seminars conducted by the leading metrological institutions of the country (VNIIMS, VNIYM. D. I. Mendeleev); - participation in contests, metrology competitions; - study of periodicals by metrology - the active use of the electronic database equipped with a flexible information search system and automatically updated as new information appears: - On the technical characteristics of measuring instruments made to the State Register and approved; - about the calibration and repair work carried out by state metrological services of legal entities; - on regulatory and reference documents in the field of metrology; - on the standards and installations of the highest accuracy; - Electronic directories of outputs.

MO carry out the following divisions of the enterprise: - the main metrologist; - the head of the chief designer; - the main technologist; -the test laboratory; - technical control; -Tell standardization; - mining production units; -Existence of auxiliary production, developing and manufacturing measurement and control tools.

MO carry out the following divisions of the enterprise: - the main metrologist; - the head of the chief designer; - the main technologist; -the test laboratory; - technical control; -Tell standardization; - mining production units; -Existence of auxiliary production, developing and manufacturing measurement and control tools.

Elements of costs of MO: § costs related to the development and improvement of control-measuring equipment; § Calibration costs of measuring equipment; § Costs for templates, samples; § costs for metrological examination of design and technological documentation; § Costs for metrological control.

Elements of costs of MO: § costs related to the development and improvement of control-measuring equipment; § Calibration costs of measuring equipment; § Costs for templates, samples; § costs for metrological examination of design and technological documentation; § Costs for metrological control.

Sources of economic effect are: § Reducing losses as a result of improving the reliability and accuracy of measurements; § as a result of reducing the cost of acquisition and maintenance of measuring instruments used in the enterprise; § Reducing the current costs of performing control and measuring operations.

Sources of economic effect are: § Reducing losses as a result of improving the reliability and accuracy of measurements; § as a result of reducing the cost of acquisition and maintenance of measuring instruments used in the enterprise; § Reducing the current costs of performing control and measuring operations.

Examples of calculating costs for quality 1. Metrological examination of the design documentation 3 \u003d F · K · KN where: F - Fund for the remuneration of employees of the metrological surveillance sector; To - the coefficient that determines the part of working time spent by employees of the metrological supervision sector to perform the work on the metrological examination of the design documentation; KN - the accrual ratio on the wage foundation. C 1 - Investments

Examples of calculating costs for quality 1. Metrological examination of the design documentation 3 \u003d F · K · KN where: F - Fund for the remuneration of employees of the metrological surveillance sector; To - the coefficient that determines the part of working time spent by employees of the metrological supervision sector to perform the work on the metrological examination of the design documentation; KN - the accrual ratio on the wage foundation. C 1 - Investments

Examples of calculating costs for quality 2. Costs for calibration and primary certification of measuring instruments and test equipment 3 \u003d 31 + 32, where: 31 - payment to external organizations for metrological work; C 2 - travel expenses OGM. C 1 - Investments

Examples of calculating costs for quality 2. Costs for calibration and primary certification of measuring instruments and test equipment 3 \u003d 31 + 32, where: 31 - payment to external organizations for metrological work; C 2 - travel expenses OGM. C 1 - Investments

Examples of calculation of costs 3. Costs for warranty repair of products 3 \u003d F · K · KN + (31 +32) Where: F - Wage Fund of employees of the warranty and post-warranty repair department (ORP); To - the coefficient that determines the part of the working time spent by the staff of the ORP to perform work on the warranty repair of products; Kn - accrual coefficient; 31 - Travel expenses of OrP staff; 32 - the cost of material, nodes and blocks, etc., used for warranty repair of products. With 4 - losses from non-compliance with product requirements

Examples of calculation of costs 3. Costs for warranty repair of products 3 \u003d F · K · KN + (31 +32) Where: F - Wage Fund of employees of the warranty and post-warranty repair department (ORP); To - the coefficient that determines the part of the working time spent by the staff of the ORP to perform work on the warranty repair of products; Kn - accrual coefficient; 31 - Travel expenses of OrP staff; 32 - the cost of material, nodes and blocks, etc., used for warranty repair of products. With 4 - losses from non-compliance with product requirements

Decomposition costs for the development, production and operation of measuring instruments are divided into two components: Ø SPR - costs for the development and manufacture of measuring instruments; Ø IE - current operating costs. In turn, IE are divided: § C n - costs for s / n § Self-absorption deductions § § cp - repairs and verification costs

Decomposition costs for the development, production and operation of measuring instruments are divided into two components: Ø SPR - costs for the development and manufacture of measuring instruments; Ø IE - current operating costs. In turn, IE are divided: § C n - costs for s / n § Self-absorption deductions § § cp - repairs and verification costs

A group of quality indicators that affect the measurement error: quoted1 \u003e\u003e\u003e\u003e destinations, reliability, durability, maintainability, persistence, ergonomic, aesthetic, manufacturability, transportability,\u003e Standardization and unification,\u003e patent-headed,\u003e security,\u003e homogeneity,\u003e influences on Environment,\u003e External Sustainability.

A group of quality indicators that affect the measurement error: quoted1 \u003e\u003e\u003e\u003e destinations, reliability, durability, maintainability, persistence, ergonomic, aesthetic, manufacturability, transportability,\u003e Standardization and unification,\u003e patent-headed,\u003e security,\u003e homogeneity,\u003e influences on Environment,\u003e External Sustainability.

The relationship of quality indicators with the effect of quality indicators In which components are reflected 3 PR szp EE itself, the purpose of the destination: Performance Measurement Range Measurement Performance Indicators Reliability Indicators: + Understandability Durability Referenceability Saveability Indicators: Employment Indicators + + + +

The relationship of quality indicators with the effect of quality indicators In which components are reflected 3 PR szp EE itself, the purpose of the destination: Performance Measurement Range Measurement Performance Indicators Reliability Indicators: + Understandability Durability Referenceability Saveability Indicators: Employment Indicators + + + +

Improving the accuracy of measurements: Improving the reliability of measurements, tests and controls may be the result of such events as improving the processes of calibration or a decrease in intermediate intervals; Introduction of standard samples of substances and materials for operational control of the measurement correctness, etc.

Improving the accuracy of measurements: Improving the reliability of measurements, tests and controls may be the result of such events as improving the processes of calibration or a decrease in intermediate intervals; Introduction of standard samples of substances and materials for operational control of the measurement correctness, etc.

In determining the metrological costs, it is necessary to estimate: 1) 2) 3) costs directly to the measurement; the cost of metrological maintenance of measuring instruments; Losses due to measurement errors.

In determining the metrological costs, it is necessary to estimate: 1) 2) 3) costs directly to the measurement; the cost of metrological maintenance of measuring instruments; Losses due to measurement errors.

1. Costs directly on measuring research costs; the cost of metrological certification; costs for the purchase of measuring instruments; Costs for installation of measuring instruments. costs for calibration of measuring instruments; costs for monitoring the performance of measuring instruments; costs for approval of the type of measuring instruments; Costs for current repair of measuring instruments.

1. Costs directly on measuring research costs; the cost of metrological certification; costs for the purchase of measuring instruments; Costs for installation of measuring instruments. costs for calibration of measuring instruments; costs for monitoring the performance of measuring instruments; costs for approval of the type of measuring instruments; Costs for current repair of measuring instruments.

2. The cost of metrological maintenance of measuring instruments is the cost of measuring measurement and standards in the state metrological service. Their value is determined based on the tariffs of these bodies and transportation costs.

2. The cost of metrological maintenance of measuring instruments is the cost of measuring measurement and standards in the state metrological service. Their value is determined based on the tariffs of these bodies and transportation costs.

One of the main elements of MO is the technical means of metrological support, including: § standards, § Exemplary and § working means of measurements.

One of the main elements of MO is the technical means of metrological support, including: § standards, § Exemplary and § working means of measurements.

3. Losses due to measurement errors Indicator of losses from measurement error: - Economic losses from false marriages of standards; - Economic losses from false variance of measuring instruments; - People's business losses. The convenience of presenting losses in the form of the three terms is that it is possible to use only those constitutions that are needed in this case.

3. Losses due to measurement errors Indicator of losses from measurement error: - Economic losses from false marriages of standards; - Economic losses from false variance of measuring instruments; - People's business losses. The convenience of presenting losses in the form of the three terms is that it is possible to use only those constitutions that are needed in this case.

Scheme of economic losses from measurements Measurement Estate the cost of SET Economic losses for exemplary measurement means Costs from government tests and metrological certification about economic losses of PR Working Means of measurements The need for production in reliable measuring information The nomenclature of the measurement of the parameters of the parameters value and the allowable response of the requirements for the parameters The accuracy of measurements to the requirements of the operation of obtaining information of the measurement methods is not realization of measurement processes Costs of the CIZ Certification (choice) Meeting Meetings Meeting Metrological examination of technical documentation Measuring information National Economic Economic Losses from the PNH measurement error

Scheme of economic losses from measurements Measurement Estate the cost of SET Economic losses for exemplary measurement means Costs from government tests and metrological certification about economic losses of PR Working Means of measurements The need for production in reliable measuring information The nomenclature of the measurement of the parameters of the parameters value and the allowable response of the requirements for the parameters The accuracy of measurements to the requirements of the operation of obtaining information of the measurement methods is not realization of measurement processes Costs of the CIZ Certification (choice) Meeting Meetings Meeting Metrological examination of technical documentation Measuring information National Economic Economic Losses from the PNH measurement error

Diagram of the relationship of solved measuring tasks and parameters of the elements of the production process Measurement processes Measuring control Parameters of the expendability of its resource being spent using flow measurement, when taking into account and dosing the parameters of the technological process Parameters of materials, raw materials of energy, component measurement elements when controlling technological processes of technological equipment , snap, tool People's economic losses from the measurement error in PNH

Diagram of the relationship of solved measuring tasks and parameters of the elements of the production process Measurement processes Measuring control Parameters of the expendability of its resource being spent using flow measurement, when taking into account and dosing the parameters of the technological process Parameters of materials, raw materials of energy, component measurement elements when controlling technological processes of technological equipment , snap, tool People's economic losses from the measurement error in PNH

Indicators of economic efficiency of work on MO: Mi 2546 -1999 "Methods for determining the economic efficiency of metrological works" establishes the system of indicators and methods for determining the effectiveness of work on metrological support.

Indicators of economic efficiency of work on MO: Mi 2546 -1999 "Methods for determining the economic efficiency of metrological works" establishes the system of indicators and methods for determining the effectiveness of work on metrological support.

2 types of indicators were established: the indicators of general economic efficiency are expressed in the form of an increase in profit growth (reduction of production costs) to the costs that caused this increase: net discounted income (integral effect); return index; Internal rate of income; payback period. Comparative performance indicators that are applied to the economic rationale and choose the best options for the implementation and use of new techniques: - Costs.

2 types of indicators were established: the indicators of general economic efficiency are expressed in the form of an increase in profit growth (reduction of production costs) to the costs that caused this increase: net discounted income (integral effect); return index; Internal rate of income; payback period. Comparative performance indicators that are applied to the economic rationale and choose the best options for the implementation and use of new techniques: - Costs.

Methods and results of improving metrological problems 1. Creating a regulatory framework for optimal measurement accuracy will allow you to switch to optimization of metrological support of production in general. 2. Creation of a methodological document on optimizing testing schemes. The basis of improving and improving the efficiency of the State Metrological Service 3. The preservation of state supervision will make it possible to create guarantees of social justice, protect the rights of consumers from the manufacturer's dictate under deficiency conditions.

Methods and results of improving metrological problems 1. Creating a regulatory framework for optimal measurement accuracy will allow you to switch to optimization of metrological support of production in general. 2. Creation of a methodological document on optimizing testing schemes. The basis of improving and improving the efficiency of the State Metrological Service 3. The preservation of state supervision will make it possible to create guarantees of social justice, protect the rights of consumers from the manufacturer's dictate under deficiency conditions.

General provisions, determining the economic efficiency of metrological support of production.

The mechanism for the formation of economic losses from the measurement error.

General determination of metrological costs.

Methods for calculating the economic effect of work on Mob.

Calculation of the value of metrological works conducted by state standard authorities.

Economic efficiency of introducing new methods and measuring instruments.

The economic effect of the certification of non-standardized measuring instruments, technological, control and measuring and test equipment.

The economic effect of the introduction of working standards and calibration equipment.

Economic efficiency.

Another important task is a single metrology that allows to assess the economic efficiency of the implementation of metrological support programs.

The actual and expected economic effect is calculated by the method of comparative efficiency, according to which the effect size is defined as the cost difference in basic and implemented options.

Let us analyze the applicability of this method to assess the effectiveness of metrological support at the program development stage, i.e. When planning and when evaluating the actual effect. To do this, consider the expression of the absolute effect as the difference between the result and the costs of its achievement. The result is a fixed value.

Suppose there are two options for the plan. The absolute economic effect on the first and second options is as follows:

|

|

where - a useful result due to metrological support activities; - valuation costs for the implementation of measures for metrological support on the first and second options of the plan, respectively.

Since work on metrological support is part of work on improving product quality and production efficiency, they can be distinguished by a part of the useful result of production, i.e. , where is the beneficial result of production; - the coefficient of shared participation of work on metrological support in the general useful result of production.

In this case, we are not interested in the definition method, because Further reasoning from this does not depend.

Inequalities (1.2.1, 1.2.2) mean that both options are effective and achievable result is the same. If, then the best is the second option.

When choosing the metrological support options, this case is possible when one of them gives a negative effect.

As we suggested, then

|

| |

|

|

Here is also better than the second option. Consider whether the situation described by inequalities (1.2.1-1.2.4) is applicable to the situation (1.2.1-1.2.4), the comparative efficiency method based on comparison of costs by options. For this, the expression (1.2.1) is submitted from formula (1.2.2). We get a comparative effect

At the same time, the value (useful result) will be reduced and the formula of comparative efficiency will be obtained using the cost difference. If, TOI results of calculations using formulas (1.2.1, 1.2.2) and expression (1.2.5) allow you to take the same solution to select a better option. Similarly, inequalities (1.2.3, 1.2.4) also confirm that the second option is better.

This means that when the absolute economic effect of at least one option is positive, the methods of absolute and comparative efficiency give the same result when choosing a better option.

Another situation occurs when considering the case when both options for work plan for metrological support are economically inappropriate, i.e.:

|

| |

|

|

If, then, again, the second option is preferable. In this case, it can seems to be the effect on cost difference, as established by formula (1.2.5). But if the effect is evaluated according to this formula, then its value will be positive, because on the other hand, both options are ineffective in accordance with inequalities (1.2.6, 1.2.7). Consequently, when obtaining negative values \u200b\u200bof absolute economic effects, the comparative efficiency method is not applicable, since in accordance with it mistakenly justify the effectiveness of the "bad" version among the many "very bad". Therefore, a method based on comparing costs, when planning work on metrological support and choosing the best option, it is necessary to supplement the condition for checking the positivity of absolute effects for all alternative options.

Such a check can be carried out very close methods, since it is necessary to install the size of the effect, but only the sign of this value. All options with a positive effect include potentially possible, and then the best is chosen by cost differences. In this case, a useful result should be permanent. If this provision is not observed, then in the formation of programs and metrological plans, it is necessary to use the method of absolute efficiency. This condition is a guarantee of the effectiveness of planned measures for metrological support, since The result always exceeds the costs of achieving it.

Specificity programs, which means both metrological provision programs, is that their effect is not assessed by the amount of effects from the implementation of tasks, in them incoming.

At the same time, the "Program Effect" itself must also be taken into account, due to the following factors:

Reducing the level of duplication of work;

The presence of mutual correlation when any development in the metrological support should be carried out in the complex on the other;

The system of the program determined by the well-known position of the system analysis is "the whole amount of the components of its parts". At the same time, the accounting of the interconnection of work on the metrological support and the system factor is an unexplored task, the solution of which must be outlined.

One of these paths is to highlight the "blocks" of programs containing a number of interrelated work.

The effectiveness of such a block is estimated by the final result, and then the effect is divided according to the equity participation of each work.

Thus, as a result of the consideration of the economic aspects of the work on the analysis of the measurement status and program-targeted planning of the metrological provision of production, it is possible to conclude about the relevance and practical feasibility of conducting research in the directions:

Metrology formation of the final result of metrological maintenance of production;

Establishment of the effect of measurement accuracy for technical and economic production indicators;

Substantiation of the criterion for the effectiveness of metrological support of production;

The creation of the scientific and methodological foundations for assessing the economic efficiency of work on metrological support of continuous measuring processes;

Optimization of the nomenclature of measured parameters and accuracy of measurements for the economic criterion;

The main of these areas is the first, because It allows you to allocate from the total final result of production, the share due to the activities on metrological support. When carrying out the other listed studies, the final result indicator will also be part of the criterion.

Designed VNIIMS.

EXECUTOR Kulik K.V.