CTP Supreme Court. Resolution of the Plenum of the Supreme Court on CTP. The Supreme Court of the Russian Federation has updated clarifications on the application of the law on civil liability insurance

Resolution of the Plenum of the Supreme Court of the Russian Federation No. 2 "On the application by courts of legislation on compulsory insurance of civil liability of vehicle owners" was adopted on January 29, 2015, and since then the courts have been actively using it in this frequent category of disputes. What explanations are used most often, what mistakes are canceled by higher authorities, what is judicial practice understood as abuse in the field of insurance claims? The answers to these questions are - in a selection of cases compiled using Caselook, in which the regional courts applied Plenum ruling # 2.

What explanations were most useful

Among the most frequently used clarifications of the regulation- p. 32, which from October 17, 2014 obliges to calculate insurance compensation according to a unified methodology, which was approved by the Central Bank (regulationNo. 432-P dated September 19, 2014). Higher courts advise not to forget about the instructions in this document, which may affect the outcome of the case. In particular, a discrepancy in calculations of 10% or less is considered a statistical error. Therefore, the courts must reject the claims of motorists that require 10% or less of the actually paid sum insured (for example, case No. 33-19993 / 16 in the Krasnodar Regional Court).

Some of the “popular” provisions of the Plenum draw the courts' attention to some changes in the legislation on OSAGO, which have been in effect since September 1, 2014. From this day, the pre-trial procedure for resolving disputes (clause 7) and a twenty-day period for considering the victim's application are in effect. If the company did not meet the payment within this deadline, a penalty of 1% per day of delay is charged on it (clause 21 of article 12 of the Law on OSAGO), but only if the contract was concluded not earlier than September 1, 2014, pays attention to clause 44 And if earlier, it is necessary to use other rules, which have been established by Art. 13 about OSAGO. It happens that the courts do not pay attention to the date of the conclusion of the contract and mistakenly apply the old rules to new contracts or vice versa. Higher authorities correct them (for example, case No.33-3045 / 2017 of the Krasnoyarsk Regional Court).

When something is wrong with the documents

It also happens that it is not clear from the police documents what is the fault of the insured person or each of the drivers in the accident. But this is not yet a reason to refuse insurance compensation, recalls paragraph 21 of the Plenum's resolution. It was applied by the Rostov Regional Court, which overturned the decision of the Taganrog City Court, which decided not to punish the ENI insurance company. Although Pyotr Dolbakov * had to collect 340,400 rubles for the repair of the "Folsquagen Tiguan" through the court, the first instance denied him a penalty and a fine. After all, Dolbakov did not attach proof of the guilt of another participant in the accident to the application for payment, but provided them later. But the insurance company does not justify this, objected the appeal and referred to paragraph 21 of the Resolution. If, according to the documents, it is difficult to determine the guilt of the insured person or each of the drivers, the organization must pay in equal shares of the amount of damage suffered by each - the resolution of the Plenum resembles par. 4 p. 22 art. 12 of the law on OSAGO. According to the decision of the appeal, the driver received in addition 371,632 rubles. forfeit and fine (33-1552 / 2017).

It's another matter if the car owner has not submitted all the necessary documents to the insurance company. This can exempt the insurer from paying forfeits and financial sanctions if he proves that he has violated the terms due to force majeure or guilty actions (inaction) of the victim, says paragraph 58 of the resolution (applied, for example, in the case of the Sverdlovsk Regional Court No. 33-5911 / 2017 ). The most common mistake of victims is not submitting all the necessary documents to the insurance company. "I forgot; I thought I sent it; I thought it didn't matter," the plaintiffs explain to the court. But t such frivolity can be costly, as happened with Irina Kuderova *, who was hit by a car on a zebra crossing. She was forced to undergo treatment at the hospital, where it was determined that she had received moderate harm to her health. But it was not possible to receive a refund from the Russian Union of Auto Insurers: Kuderova did not submit all the necessary documents that were required according to the law on MTPL and insurance rules (in particular, there was not enough copy of the passport). A month and a half later, when the victim filed a pre-trial claim, she was reminded of the shortage. She again ignored the remark and went to court.

Quite often, a fine is denied because the policyholder intentionally does not provide the car for inspection. The Military Insurance Company accused Takhir Shahazadov * of such abuse, who was seeking compensation after the accident of his Mercedes. Employees of the "VSK" twice sent him telegrams with the dates and places of the inspection, but Shahazadov did not bring his car. He did this only the third time and finally received compensation, the amount of which he was dissatisfied with. The court managed to get more compensation, but the fine was refused (2-1023 \\ 2017). The Dzerzhinsky District Court of Volgograd agreed that Shahazadov had abused his right by not presenting the car for inspection.

And here is the Volgograd Regional Court came to the opposite conclusion and drew attention to the details that spoke of the driver's innocence. Indeed, the case file contained telegrams, but there was no confirmation that they had been received. Moreover, in the official statement that the car was not presented, the VSK employee indicated a different address than the one in the message. Therefore, Shahazadov has every right to receive a fine, the appeal concluded (33-6643/2017).

Unusual abuse discoveredBelgorod Regional Court in case 33-1393 / 2017. He refused to buy up insurance debts Igor Krolchev * to receive a forfeit and a fine, which the plaintiff was awarded by the first instance. According to her decision, Krolchev received 93,189 rubles. insurance payment and 85 706 rubles. as financial sanctions for non-payment of the premium. The defendant did not admit his guilt and explained that the plaintiff demanded payment in cash in Belgorod as well. But the company did not have a cash desk in this city, and Krolchev refused to go to Moscow or provide the account details. The regional court did not agree with the first instance that “Max” was obliged to issue cash in Belgorod, on the contrary, there were no obstacles to receiving payment from the creditor. The appeal noted that Krolchev systematically demanded cash from the company in Belgorod, although he knows perfectly well that there is no cash desk there. Therefore, he was denied a penalty and a fine.

Stolen policy: what to do?

What to do if a bona fide policyholder has an invalid policy, says paragraph 15 of the Plenum. The company may not pay for it only if, before the date of the insured event, the insurer, broker or agent applied to the authorized bodies with a statement about the theft of forms (clause 7 of Art. 15 of the Law on OSAGO ). This clarification appliedMoscow Regional Court canceling the decisionDomodedovo City Court on the recovery of 120,000 rubles. with Liberty Insurance in favor of Igor Sofonov * (33-32263 / 2016). The fact is that the "insurance" accident happened on January 29, 2014, and six months before that, in July 2013, the company told law enforcement agencies that the director of the intermediary, Favorit LLC, had stolen the forms, among which there was then Sofonov's policy ... "Information about the loss of the policy is also indicated in the notification on the official website of the Russian Union of Auto Insurers," the definition says. Thus, the appeal denied the plaintiff and decided not to recover compensation from the company.

Most recently, the Supreme Court of the Russian Federation has finished preparing a review of judicial practices, which will be obligatory for review by absolutely all employees of courts of all instances. In this document, employees of the RF Armed Forces say that this document will play an important role in resolving conflict situations in the field of insurance services.

Dear Readers! The article talks about typical ways of solving legal issues, but each case is individual. If you want to know how to solve your problem - contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and WITHOUT DAYS.

It is fast and IS FREE!

In the course of work on this document, special attention was paid to judicial practices, which were aimed at resolving conflicts related to road accidents, in which the drivers became participants in a state of intoxication.

The VS also expanded and clarified the term "other vehicles", which is used in matters of vehicle theft. This term includes such means of transportation as buses, trams, trolleybuses, two-wheeled motorized vehicles (moped, motorcycle), tractors, and also water vehicles (boats, etc.).

However, it was clarified that this addition is applicable only in cases where only theft was committed, without another corpus delicti: theft or embezzlement. An attempt was also made to equate theft with theft, but it was not crowned with success.

Moreover, the Supreme Court ruled that compensation for the hijacked vehicle must be paid without deducting the depreciation of the vehicle that was caused during its operation.

Innovations

The 2019 CTP plenum was amended and supplemented during the work of the Armed Forces of the Russian Federation.

In general, the following points of changes were the most important:

- obligatory implementation of pre-trial (claim) procedures for resolving conflicts in cases of insurance payments that occurred after September 1, 2019;

- expanding the scope, which now include the operation of the vehicle in the adjacent territory, during towing, parking, etc .;

- reimbursement of the loss of commodity value has become mandatory;

- the possibility of paying for losses that were incurred due to the loss or damage to the goods;

- the imposition of a fine in the amount of half of the unpaid amount of insurance is required, despite the existence of requirements for its payment;

- the possibility of transferring the rights to receive insurance payments to another citizen;

In the course of its work, the VS made a number of important decisions that will significantly affect the principle of cooperation with insurance companies in the near future.

Issues raised

During the plenum on compulsory motor third party liability insurance, a number of issues were clarified, which caused many disputes in the past. Already today, there are documents that control the legal relations on compulsory motor third party liability insurance among various persons, the limitation period has been discussed, the specifics of considering all legal disputes on compulsory motor third party liability insurance have been clarified, and the amount of insurance payments has been clarified.

According to officials, these issues often caused conflicts between citizens and insurance companies, which often resulted in litigation. These documents are aimed at reducing the number of "gaps" in modern laws in order to minimize the occurrence of such situations.

They can significantly reduce the base cost of the policy, therefore, the final price of OSAGO can be found out only after providing full information on the personality of the driver and the technical characteristics of the car.

How MTPL for legal entities differs from MTPL for individuals, read in.

Approval of dispute procedures

In the course of its work, the Supreme Court of the Russian Federation introduced a number of important changes to the regulation of the insurance field of vehicles. According to representatives of the law, this move is aimed at minimizing the role of the courts in disputes between insurance agencies and motorists, since it is often the courts that are used to make unlawful decisions for one side or another.

Many experts argue that these changes should deprive the financial profit of the companies that buy the rights to the victims from the victims, because then unscrupulous law firms try to maximize the volume of insurance payments from insurance agencies, supplementing insurance premiums with amounts for moral damage and for late payment of payments. The amended law states that it is now necessary to notify the insurer of existing insurance claims in a pre-trial manner.

All these changes, according to lawyers, should have a favorable effect on the state of the modern market, reducing the number of financial losses of insurance companies, which in the future should lead to a significant reduction in the cost of compulsory motor third party liability insurance for individuals.

Compromise for everyone

As a recent survey of both motorists and representatives of insurance companies shows, absolutely everyone liked the decision of the recent plenum. Thanks to the well-coordinated work of all parties, the quality of the document satisfied all parties, which was, perhaps, the first case in recent years.

According to preliminary calculations, the 2019 CTP plenum will allow to almost halve the number of legal conflicts. Insurance companies are delighted that the Supreme Court has allowed insurance disputes to be resolved out of court.

If, during the initial appeal of the motorist, the decision of his insurance representative was not satisfied, then during 5 days he has the opportunity to re-submit a claim to his insurer. If the driver is repeatedly not satisfied with the decision, then the dispute is sent to the court.

In addition, the Supreme Court has also issued a number of decisions that make life much easier for motorists. For example, a driver has the right to use his vehicle for up to 10 days without a compulsory insurance policy from the date of purchase, and he will not be subject to penalties from the inspection authorities.

If in the course of the accident road infrastructure objects were damaged, then the company providing insurance services to the driver will be obliged to pay the full amount of compensation to the company that is responsible for the condition of this section of the road. This decision seems to the drivers fairly fair, as they were happy to inform many sources.

As mentioned above, the concept of loss of the market value of a vehicle was introduced, which must be compensated by the insurance company, but the amount of compensation can only be established in court. Insurance services are concerned about this situation, since they have not yet developed a methodology for calculating the volume of TCB, which, as a result, may lead to the emergence of new schemes of financial fraud in this area.

Representatives of the Central Bank of the Russian Federation claim that work on such methods is being carried out very actively at the moment, and in the near future they will be ready for active use in daily court practice.

New policy and fakes

During the work of the plenum on OSAGO it was mentioned that the insurance policy belongs to the strictest form of reporting. It follows from this statement that the manufacture and sale of counterfeit OSAGO policies is punishable by criminal liability under the relevant article (Article 327 of the Criminal Code of the Russian Federation).

It was mentioned that due to the increase in the number of counterfeit policies in the modern auto insurance market, it is necessary to introduce more precise control in this area of \u200b\u200bdocument flow.

Motorists were given a lot of advice on how to avoid problems with acquiring fake policies, but the most important advice was to buy insurance only from trusted insurance agents. In this case, the car owner minimizes the likelihood of acquiring a fake and can protect himself from conflict situations with the insurance company in the future.

It was mentioned more than once that it would soon be necessary to replace the policies with new and more modern and protected samples, but there was no official information on this issue from verified persons. That is why you should not rush today to replace your insurance certificate.

Despite the existence of a problem with insurance policies, it is the driver's responsibility to acquire and use a fake license.

Among the punishments for such an offense, the following are distinguished:

- depriving the driver of existing discounts for an accident-free driving experience;

- penalties for driving without an OSAGO policy in the amount of up to 800 rubles;

- in the event of an accident, such a driver will be obliged to independently reimburse the amount of damage to the victim in case of proof of his guilt;

- if an attempt is detected to receive material payments on an invalid insurance certificate, it is possible to apply criminal sanctions, up to the initiation of a criminal case;

Resolution of the plenum on OSAGO in 2019

So, in order to ensure more complete control of the sphere of insurance activities of both companies providing insurance services and drivers who are consumers of such services, the RF Armed Forces issued a number of decrees that significantly affect the interaction of both parties.

OVERVIEW

PRACTICES OF CONSIDERATION BY THE COURTS OF CASES RELATING TO THE OBLIGATORY

OWNER'S LIABILITY INSURANCE

VEHICLEThe Supreme Court of the Russian Federation studied the issues received from courts of general jurisdiction and arbitration courts, as well as summarized certain materials of judicial practice related to compulsory civil liability insurance of vehicle owners.

When considering cases related to compulsory civil liability insurance of vehicle owners, the courts were guided by:

Subrogation

23. Expenses for the examination (appraisal) of a vehicle shall be recovered from the insurer as losses

Insurer's liability

24. Penalty and financial sanction for violation of the term of insurance payment under OSAGO is calculated from 21 days

25. The penalty under the law on OSAGO is charged for the amount of repairs and other expenses, incl. to evacuate the vehicle from the accident scene

26. Payment of insurance indemnity under OSAGO during a dispute in court does not exempt the insurer from a fine

27. Consequences of refusal to pay insurance compensation under OSAGO in the event that the insurer is presented with the necessary documents

28. Reduction of penalties for compulsory motor third party liability insurance, financial sanctions, fine under Art. 333 of the Civil Code of the Russian Federation

29. Refusal to collect a penalty for compulsory motor third party liability insurance, a fine, moral harm in case of abuse of the right

Many years have passed since the introduction of the compulsory car insurance system in Russia, but it can be stated that some aspects of judicial practice in resolving disputes related to the Law on Compulsory MTPL still have ambiguous interpretations. The conflict of interests between the insurer and the driver is far from always resolved in a "peaceful" way, mutually beneficial for the parties. Many controversial provisions have to be considered in the judicial authorities of the Russian Federation in order to deliver a final and irrevocable verdict.

Plenum of the Supreme Court on OSAGO 2015

Unfortunately, the court decisions were not always equivalent for similar cases, revealing the imperfection of Russian legislation. To eliminate distortions in judicial practice and ambiguous interpretations of the applied articles, the Supreme Court of the Russian Federation (RF Armed Forces) held a special Plenum devoted to the accumulated controversial issues related to compulsory motor third party liability insurance.

As a result of the Plenum of the RF Armed Forces held on January 29, 2015, a resolution was adopted, which is, in fact, a set of lawful court decisions in a particular disputable situation and clarifying the scope of their application. Let us examine some of the important points that were considered at the Plenum of the Armed Forces on OSAGO.

Topics of the Plenum of the RF Armed Forces dated 01.29.2015

Plenum No. 2 on OSAGO considered materials and summarized judicial practice on the following issues:

- Legal regulation of relations on compulsory civil liability insurance of vehicle owners.

- Procedural features of consideration of cases on compulsory civil liability insurance of vehicle owners.

- Limitation of actions.

- Compulsory civil liability insurance contract for vehicle owners.

- Insurance payment.

- Measures of the insurer's liability for violation of the terms of payment of insurance compensation.

The explanations were fixed in the form of the Resolution of the Plenum of the RF Armed Forces.

Resolution of the Plenum of CTP

Here are the main conclusions from the Resolution, which should be given special attention:

- The obligation of the insurance company is not only to reimburse the damage caused as a result of an accident, but also to compensate for the loss of the vehicle's market value.

The Supreme Court quite definitely ruled to consider the loss of commodity value as actual material damage. In such a case, compensation for damage to the car owner by an insurance company can be carried out in two ways: by transferring funds or by sending the damaged car for service repair.

- The procedure for compensation for damage for the mutual fault of the participants in the accident.

In cases of violation of traffic rules by both participants and their recognition by the traffic police as the culprit, the RF Armed Forces were recommended to establish the degree of guilt of each of the drivers and to make insurance payments depending on this degree. If the degree is not determined, compensation will be no more than 50% of the cost of the repair costs.

- Payment of compensation for damage to the car, received off the carriageway.

The Armed Forces of the Russian Federation at the Plenum on MTPL drew attention to the legality of the statement of the motorist injured in this way about the payment by the insurer of material compensation for damage, which previously excluded such a practice - all accidents that happened in yards or in parking lots were categorically not recognized as an insured event.

- The responsibility of the insurance company for the proper quality of repairs to the victim's car, made in a car service in the direction of the insurer.

At the plenum, special attention was paid to the division of responsibility when carrying out repair work in the service. As before, the entire responsibility for the quality of the repair falls on the car service, and the victim has the right to contact his insurance company in case of revealing post-repair problems for their elimination.

- In the event of damage to property other than a vehicle (gas station property, building or other), the damage assessment is determined by estimates, the opinion of the appraiser and other settlement documents.

According to the Resolution adopted at the Plenum on OSAGO, insurance companies can be involved in monetary payments to compensate for justified damage in cases of damage to real property, namely, in case of damage to gas station equipment, residential and non-residential buildings near the roadway, fences, fences, poles, etc.

- Direct settlement between the OSAGO insurer and the victim of road traffic accidents involving no more than 2 vehicles and without causing physical injury.

The Armed Forces of the Russian Federation approved a direct pre-trial settlement in some emergency cases, when the first step of the party injured in an accident should be to apply with a proper application to its insurance company.

- The occurrence of an insured event can be recorded in other cases other than the independent movement of the vehicle, namely, when it is parked, towed, stopped, etc.

Insurance companies were obliged, in contrast to the previous period, to apply the legalized mechanism of material payments not only in cases of road traffic accidents, but also in emergency cases of its immovable condition or towing.

- With the consent of the victim, monetary compensation can be replaced by the insurance company with a referral for repairs to a car service, and the wear of units and auto parts is paid by the victim.

The CTP plenum ruled that in cases of road traffic accidents in which the final loss of the vehicle is not confirmed, but repairable damage has been caused, the injured party has the right to choose - either the insurance company will pay monetary compensation or repair in a car service at the expense of the insurer.

- Application of an increased amount of insurance payments: up to 400 thousand rubles in case of damage to a vehicle in an accident and up to 500 thousand rubles in case of injury to health in an accident, respectively.

All points of the Resolution of the Plenum of the RF Armed Forces on OSAGO can be found below.

Results of the Plenum of 01/29/2015

In its resolution, the Plenum on MTPL outlined the timing of the introduction in 2015 of new maximum monetary compensation for damage in a road traffic accident, which are still valid.

It should be noted that the Plenum of the Supreme Court considered and passed its undeniable verdict on many controversial issues and became a significant event in the further development of the domestic OSAGO system.

The Plenum significantly expanded the area of \u200b\u200bresponsibility of insurers, defined a clear algorithm for the parties to act in a given situation, predetermined new maximum payments and specified some terms. Most of the decisions adopted at the Plenum on MTPL on the implementation of insurance practice and the legislative resolution of disputes are still valid today.

a) cases on property disputes (for example, in the case of a claim for the recovery of an insurance payment) with a claim price not exceeding fifty thousand rubles on the day of filing the application, are subject to the jurisdiction of the magistrate (clause 5 of part 1 of article 23 of the Code of Civil Procedure of the Russian Federation);

b) cases on property disputes with a claim price exceeding fifty thousand rubles on the day of filing the application, as well as cases on claims that are not subject to assessment (for example, on violation of the consumer's right to reliable information) are subject to the jurisdiction of the district court (Code of Civil Procedure of the Russian Federation).

In the event that, simultaneously with a claim of a property nature, the justice of the peace, a derivative claim for compensation for moral damage is declared, such cases are within the jurisdiction of the justice of the peace.

If, upon filing a counterclaim, the new claims are within the jurisdiction of the district court, all claims shall be subject to consideration in the district court. In this case, the magistrate makes a ruling on the transfer of the case to the district court (part 3 of article 23 of the Code of Civil Procedure of the Russian Federation).

4. Cases on disputes arising from the contract of compulsory civil liability insurance of vehicle owners and related to the implementation of entrepreneurial and other economic activities by legal entities and individual entrepreneurs are subject to consideration by an arbitration court (Part 1 of Article 27 of the Arbitration Procedure Code of the Russian Federation (hereinafter - the APC RF).

5. Cases on disputes related to compulsory civil liability insurance of vehicle owners are considered according to the general rule of territorial jurisdiction at the location of the defendant (Code of Civil Procedure of the Russian Federation, Arbitration Procedure Code of the Russian Federation).

A claim against an insurance company may also be filed at the location of the branch or representative office that has entered into a compulsory insurance contract, or at the location of the branch or representative office that has accepted an application for making an insurance payment (Part 2 of Article 29 of the Code of Civil Procedure of the Russian Federation and Part 5 of Article 36 of the APC RF).

Claims in disputes related to compensation payments are subject to consideration according to the general rules of territorial jurisdiction - at the location of the professional association of insurers or at the location of its branch or representative office.

6. When the victim files a claim directly against the inflictor of harm, the court, by virtue of part 3 of Article 40 of the Code of Civil Procedure of the Russian Federation and part 6 of Article 46 of the Arbitration Procedure Code of the Russian Federation, is obliged to involve an insurance organization as a defendant in the case, to which, in accordance with the Law on Compulsory Liability Insurance, the victim has the right to apply with a statement of insurance payment or direct compensation for losses (paragraph two of clause 2 of Article 11 of the Law on Compulsory Motor Third Party Liability Insurance).

In cases where this circumstance is established when considering a case or involving an insurance organization as a defendant, claims against both the insurer and the inflictor of harm shall be left without consideration on the basis of paragraph 2 of Article 222 of the Code of Civil Procedure of the Russian Federation and paragraph 2 of Part 1 of Article 148 of the Arbitration Procedure Code of the Russian Federation.

The rules on mandatory pre-trial settlement of a dispute are also applied in the case of replacing the defendant - the tortfeasor with an insurance company.

Limitation of actions

10. The courts must take into account that the limitation period for disputes arising from legal relations on compulsory insurance of the risk of civil liability in accordance with paragraph 2 of Article 966 of the Civil Code of the Russian Federation is three years and is calculated from the day when the victim (beneficiary) learned or should have learned about the refusal the insurer in the payment of insurance indemnity or on its payment by the insurer not in full, or from the day following the day established for making a decision on the payment of insurance indemnity (issuing a referral for vehicle repair), provided for in paragraphs 17 and 21 of Article 12 of the Law on OSAGO or by agreement.

11. The change of persons in the obligation (in particular, upon subrogation, assignment of the right of claim) for the claims that the new creditor has against the person responsible for losses caused as a result of a road traffic accident does not entail a change in the course of the total (three-year) period the limitation period and the procedure for calculating it (Civil Code of the Russian Federation).

12. The basis for interrupting the limitation period may be, in particular, the recognition of the claim by the insurer, partial payment of insurance compensation and / or penalty, financial sanction (Civil Code of the Russian Federation).

Compulsory civil liability insurance contract of vehicle owners

13. The compulsory insurance contract must comply with the Law on Compulsory MTPL and the Insurance Rules in force at the time of its conclusion. Changes to the provisions of the Law on MTPL, Insurance Rules after the conclusion of the contract does not entail changes in the provisions of the contract (in particular, on the procedure for execution, validity periods, essential conditions), except for cases when the law applies to relations arising from previously concluded contracts (paragraphs 1 and 2 Article 422 of the Civil Code of the Russian Federation).

When resolving disputes arising from compulsory civil liability insurance contracts of vehicle owners, it should be borne in mind that the rules of article 428 of the Civil Code of the Russian Federation on the contract of accession are subject to the insurance contract in the part in which it is concluded on the terms of the Insurance Rules.

The compulsory insurance contract is public, it is concluded under the conditions stipulated by the Law on Compulsory MTPL and other legal acts adopted for the purpose of its implementation.

In the event of a dispute about the content of the insurance contract, the content of the policyholder's application, the insurance policy, as well as the insurance rules on the basis of which the contract was concluded, should be taken into account.

14. The compulsory insurance contract does not apply to cases of harm to life, health and / or property when using a vehicle on the territory of a foreign state, including in the case when the amount of damage exceeds the maximum insured amount under the "green card" insurance rules (Law on OSAGO).

15. Issuance of an insurance policy is evidence confirming the conclusion of a compulsory civil liability insurance contract until proven otherwise.

Incomplete and / or untimely transfer to the insurer of the insurance premium received by the insurance broker or insurance agent, unauthorized use of compulsory insurance policy forms do not exempt the insurer from compulsory insurance contract (clause 7.1 of Article 15 of the Law on Compulsory MTPL).

In the event of the theft of forms of compulsory insurance policies, the insurance organization is exempt from paying insurance compensation only on the condition that before the date of the insured event, the insurer, insurance broker or insurance agent applied to the authorized bodies with a statement about the theft of forms (paragraph 7.1 of Article 15 of the Law on Compulsory MTPL) ...

16. After the conclusion of the compulsory insurance contract, the replacement of the vehicle specified in the compulsory insurance policy, change of the insurance period, as well as replacement of the policyholder are not allowed.

In the event of the transfer of ownership, the right of economic management or operational management of the vehicle from the insured to another person, the new owner is obliged to conclude a compulsory insurance contract for his civil liability (paragraph 2 of Article 4 of the Law on MTPL).

18. The right to receive insurance payments in terms of compensation for damage caused to property belongs to the victim - a person who owns the property on the basis of ownership or other property rights. Persons who own property on a different right (in particular, on the basis of a lease agreement or by virtue of an authority based on a power of attorney) do not have an independent right to an insurance payment in respect of property (paragraph six of Article 1 of the Law on Compulsory Motor Third Party Liability Insurance).

If the harm caused as a result of a road traffic accident is compensated not by the insurance organization of the inflictor of harm (or in the case of direct compensation for losses - by the insurance organization of the victim), but by another person, then the person who compensated for the harm has the right to compensation for losses.

The person who has compensated the injured party (the injured party, the insurance company that paid the insurance indemnity under the voluntary property insurance agreement, any other person other than the insurance organization of the injured party or the victim's insurance organization) has the right to claim against the insurer who insured the civil liability of the victim only in cases that allow direct compensation for losses (the Law on Compulsory Motor Third Party Liability Insurance). In other cases, such a requirement is presented to the insurer who has insured the civil liability of the tortfeasor.

The person who has compensated for the damage caused as a result of the insured event has the right to claim against the insurer in the amount determined in accordance with the Law on Compulsory Motor Third Party Liability Insurance. At the same time, the implementation of the transferred right of claim is carried out in accordance with the legislation of the Russian Federation in compliance with the provisions of the Law on Compulsory Motor Third Party Liability Insurance, which regulate the relationship between the victim and the insurer (paragraph 23 of Article 12 of the Law on Compulsory Third Party Liability).

19. The rights of the victim (beneficiary) under the compulsory insurance contract can be transferred to another person only in terms of compensation for damage caused to his property upon the occurrence of a specific insured event under the compulsory civil liability insurance contract of vehicle owners (Civil Code of the Russian Federation).

The transfer of the rights of the victim (beneficiary) under the compulsory insurance contract is allowed only from the moment of the occurrence of the insured event.

The rights of the victim to compensation for harm to life and health, as well as the right to compensation for moral damage and the procedural rights of the consumer cannot be transferred under the contract of assignment of claim (Civil Code of the Russian Federation).

20. The presentation by the beneficiary to the insurer of a claim for payment of insurance compensation does not preclude the assignment of the right to receive insurance compensation. In the event that the beneficiary receives the insurance payment in part, the assignment of the right to receive the insurance payment is allowed in the part not terminated by execution.

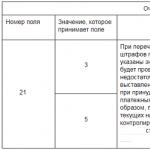

21. If it is impossible to establish the guilt of the insured person in the occurrence of an insured event from the documents drawn up by the police officers or to determine the degree of guilt of each of the drivers involved in a road traffic accident, the person who applied for the insurance payment is not deprived of the right to receive it.

In this case, insurance organizations make insurance payments in equal shares of the amount of damage incurred by each (paragraph four of clause 22 of Article 12 of the Law on MTPL).

The insurer is released from the obligation to pay a forfeit, the amount of a financial sanction, a fine and compensation for moral damage, if the obligations to pay insurance compensation in equal shares of the amount incurred by each of the drivers involved in the road traffic accident are fulfilled.

In case of disagreement with such payment, the person who received the insurance compensation has the right to apply to the court with a claim for the recovery of insurance compensation in the missing part. When considering a dispute, the court is obliged to establish the degree of guilt of the persons found responsible for the harm caused, and to recover from the insurance organization an insurance payment, taking into account the degree of guilt of the persons whose civil liability is insured established by the court. The legislation does not provide for filing an independent statement on establishing the degree of guilt.

22. The right of the original creditor is transferred to the new creditor to the extent and on the conditions that existed at the time of the transfer of the right, including the rights related to the main claim, including the right to claim against the insurer obliged to make insurance payment in accordance with the Law on MTPL , payment of a forfeit, the amount of a financial sanction and a fine (paragraph 1 of Article 384 of the Civil Code of the Russian Federation, paragraphs two and three of paragraph 21 of Article 12, paragraph 3 of Article 16.1 of the Law on Compulsory Motor Third Party Liability Insurance). The right to demand the recovery from the insurer of the fine provided for in paragraph 3 of Article 16.1 of the Law on Compulsory MTPL cannot be transferred to a legal entity until the court makes a decision on its recovery.

The same rules apply to cases of transfer to the insurer that paid the insurance compensation, the rights of claim in the order of subrogation, since such a transfer is a special case of a change of persons in the obligation on the basis of the law (subparagraph 4 of paragraph 1 of Article 387, paragraph 1 of Article 965 of the Civil Code of the Russian Federation).

23. An agreement on the assignment of the right to an insurance benefit shall be deemed concluded if the subject of the agreement is definable, ie. it is possible to establish in respect of which right (from which contract) the assignment was made. At the same time, the absence in the contract of an indication of the exact amount of the assigned right of claim is not a basis for recognizing the contract as not concluded (paragraph 1 of Article 307, paragraph 1 of Article 432, paragraph 1 of Article 384 of the Civil Code of the Russian Federation).

24. When the rights of the beneficiary (victim) are transferred to another person (for example, assignment of the right of claim, subrogation), not only the rights are transferred, but also the obligations associated with obtaining insurance compensation. The acquirer takes over the obligation to notify the insurance company of the occurrence of an insured event, which is obliged to make an insurance payment in accordance with the Law on Compulsory MTPL, to submit an application for an insurance benefit with all the necessary documents attached, to send a claim if these actions were not performed earlier by the beneficiary (victim).

25. If the amount of compensation paid by the insurer under the contract of voluntary property insurance exceeds the maximum insured amount under the contract of compulsory insurance, the right of claim is transferred to the insurer by way of subrogation, along with the right to claim against the insurance company obliged to make insurance payment in accordance with the Law on MTPL to the tortfeasor in the part exceeding this amount (Chapter 59 of the Civil Code of the Russian Federation).

26. If, when considering a case on a subrogation claim of an insurance company that paid insurance compensation under a voluntary insurance contract, against an insurance company obliged to make an insurance payment in accordance with the Law on Compulsory MTPL, it is established that the latter has paid insurance compensation under a compulsory insurance contract, then the court needs to establish which of the insurance companies made the payment earlier.

In the event that the insurance indemnity under the compulsory insurance contract was paid earlier than the insurance indemnity under the voluntary property insurance contract, then the insurer's subrogation claim under the voluntary property insurance contract against the insurer under the compulsory civil liability insurance contract is not subject to satisfaction (paragraph 1 of Article 408 of the Civil Code of the Russian Federation).

In the event that an insurance company under a voluntary property insurance contract has paid the amount of insurance compensation earlier than an insurance company under a compulsory insurance contract, the claim may be rejected if it is established that the insurance company that received the rights of the beneficiary did not properly notify the insurer of the inflictor harm about the occurred subrogation (Civil Code of the Russian Federation).

Insurance payment

27. An insurance payment is understood as a specific amount of money payable by the insurer in compensation for harm caused to the life, health and / or property of the victim (paragraph 3 of Article 10 of Law No. 4015-I, Article 1 and the Law on Compulsory Motor Third Party Liability Insurance).

Replacing the insurance payment for the restoration of a vehicle is allowed at the choice of the victim, if the damage caused to the vehicle did not lead to its complete destruction (Civil Code of the Russian Federation, paragraph 4 of article 10 of Law No. 4015-I, paragraph 15 of article 12 of the Law on OSAGO).

28. In the event of harm to the victim, recovery and other costs due to the occurrence of an insured event and necessary for the victim to exercise the right to receive insurance compensation are subject to compensation (for example, costs of evacuating a vehicle from the scene of a traffic accident, storing a damaged vehicle, delivering the victim to medical institution, restoration of a road sign and / or fence, delivery of repair materials to the place of a traffic accident, etc.).

The expenses incurred by the victim in connection with the need to restore the right violated as a result of the damage caused by the road traffic accident are subject to compensation by the insurer within the amounts established by Article 7 of the Law on Compulsory Motor Third Party Liability Insurance (clause 4 of Article 931 of the Civil Code of the Russian Federation, paragraph 8 of Article 1, paragraph one of paragraph 1 Article 12 of the Law on MTPL).

36. The issue of returning to the victim the components (parts, assemblies and assemblies) subject to replacement is essential for the correct consideration and resolution of the dispute between the victim and the insurance organization about compensation for harm in the form of organizing and paying for the restoration of the damaged vehicle at the service station, in In this connection, the court is obliged to bring this issue up for discussion by the parties (Code of Civil Procedure of the Russian Federation and the Arbitration Procedure Code of the Russian Federation).

In case of return to the victim of the components subject to replacement (parts, assemblies and assemblies), the amount of the insurance payment is reduced by their cost.

If the victim refuses to receive the components (parts, assemblies and assemblies) subject to replacement, the court is not entitled to impose on the insurer the obligation to return them to the victim.

37. In the presence of the conditions provided for the insurance payment in the order of direct compensation for losses, the victim has the right to apply for insurance payment only to the insurer who insured his civil liability (paragraph 1 of Article 14.1 and paragraph 1 of Article 12 of the Law on MTPL).

38. The simplified procedure for registration of a road traffic accident is applied if the contracts of compulsory insurance of civil liability of vehicle owners of participants in a road traffic accident were concluded from August 2, 2014 and are valid until September 30, 2019 inclusive (paragraph 4 of Article 11.1 of the Law on MTPL) ...

If at least one participant in a road traffic accident has concluded a compulsory civil liability insurance contract of vehicle owners before the specified period, the road traffic accident may be registered without the participation of authorized police officers, when the amount of damage, according to the participants in the road traffic accident, does not exceed 25,000 rubles.

39. Compensation for losses within the amounts established by Article 11.1 of the Law on MTPL is a simplified way of fulfilling the obligations of the insurer, as a result of which the payment of direct compensation terminates the obligation of the insurer and the inflictor of harm in a specific insured event (paragraph 1 of Article 408 of the Civil Code of the Russian Federation).

In this regard, the claim of the victim against the insurer and / or against the inflictor of harm for compensation for damage in an amount exceeding the maximum amount of insurance payment within the framework of the simplified procedure for registration of a road traffic accident is not subject to satisfaction, except for cases when the agreement of the participants in the road traffic accident on its registration without the participation of authorized police officers was recognized by the court as invalid.

In any case, the victim has the right to apply to the insurer who insured the liability of the person who caused the harm with a claim for compensation for harm caused to life and health that arose after the presentation of a claim for direct compensation for losses and which the victim did not know about at the time of the claim (paragraph 8 of Article 11.1 and paragraph 3 of Article 14.1 of the Law on MTPL).

47. Failure to present a damaged vehicle or other damaged property for inspection and / or for an independent technical examination, independent examination (assessment), or their repair or disposal before the insurer organizes an inspection does not entail an unconditional refusal to pay the victim insurance compensation (in whole or in part ). Such a refusal can take place only if the insurer took appropriate measures to organize an inspection of the damaged vehicle (assessment of other property), but the victim evaded it, and the absence of an inspection (assessment) did not allow to reliably establish the presence of an insured event and the amount of losses subject to compensation (paragraph 20 of Article 12 of the Law on MTPL).

48. In the event that, based on the results of the inspection of the damaged property by the insurer, the insurer and the victim have reached an agreement on the amount of insurance payment and do not insist on organizing an independent technical examination of the vehicle or an independent examination (assessment) of the damaged property, such an examination by virtue of paragraph 12 of Article 12 of the Law about OSAGO may not be carried out.

When concluding an agreement on the settlement of an insured event without an independent technical examination of the vehicle or an independent examination (assessment) of the damaged property, the victim and the insurer agree on the amount, procedure and terms of the insurance indemnity to be paid to the victim. After the insurer has made the agreed insurance payment, his obligation is considered fulfilled in full and properly, which terminates the corresponding obligation of the insurer (paragraph 1 of Article 408 of the Civil Code of the Russian Federation).

The conclusion with the insurer of an agreement on the settlement of an insured event without an independent technical examination of the vehicle or an independent examination (assessment) of the damaged property is the exercise of the victim's right to receive insurance compensation, as a result of which, after the insurer has fulfilled the obligation to pay insurance in the amount agreed by the parties, the grounds for recovery there are no additional damages. At the same time, if there are grounds for recognizing the said agreement as invalid, the victim has the right to apply to the court with a claim to challenge such an agreement and to recover the amount of insurance compensation.

49. The obligation to insure civil liability does not apply to trailers for passenger cars belonging to citizens (subparagraph "e" of paragraph 3 of Article 4 of the Law on Compulsory Motor Third Party Liability Insurance). At the same time, the obligation to insure civil liability of legal entities and citizens - owners of trailers for freight transport from September 1, 2014 is fulfilled by concluding a compulsory insurance contract, which provides for the possibility of driving a vehicle with a trailer to it, information about which is entered into the compulsory insurance policy (clause 7 article 4 of the Law on MTPL).

From October 1, 2014, i.e. from the date of the introduction of the limit sizes of the base rates of insurance rates and coefficients of insurance rates, requirements for the structure of insurance rates, as well as the procedure for their application by insurers when determining the insurance premium for compulsory civil liability insurance of vehicle owners, the damage caused by road transport accidents during the joint operation of a tractor and a trailer as part of a road train are considered caused by one vehicle (tractor), and therefore the maximum insurance payment cannot exceed the sum insured under one insurance contract, including if the owners of the tractor and the trailer are different faces.

It should be taken into account that the absence in the policy of compulsory insurance of a mark on the operation of a vehicle with a trailer, the presence of which is provided for in paragraph 7 of Article 4 of the Law on Compulsory MTPL, cannot serve as a basis for the refusal of an insurance company to make insurance payments. At the same time, in relation to subparagraph "c" of paragraph 1 of Article 14 of the Law on Compulsory MTPL, the insurer in this case has the right of recourse to the insured - the inflictor of harm.

50. The victim has the right to apply to the court with a claim against the insurance company for the payment of insurance compensation after receiving the response of the insurance company to the claim or after the expiry of the five-day period established by paragraph 1 of Article 16.1 of the Law on Compulsory MTPL for the insurer to consider a pre-trial claim, except for cases of extension of the period provided for paragraph 11 of Article 12 of the Law on MTPL.

Insurer's liability measures for violation of the terms of payment of insurance compensation

52. If one of the parties acts in bad faith in order to obtain advantages in the exercise of the rights and obligations arising from the compulsory insurance contract, the claims of this party may be denied insofar as their satisfaction would create such advantages for it (paragraph 4 Article 1 of the Civil Code of the Russian Federation).

When establishing the fact of abuse by the victim of the right, the court refuses to satisfy the claims for the collection of penalties, financial sanctions, fines and compensation for moral damage from the insurer (Articles 1 and the Civil Code of the Russian Federation).

53. When a claim is made to the court for the collection of insurance compensation, a penalty and / or financial sanction at the same time, the mandatory pre-trial procedure for resolving the dispute is considered met if the conditions provided for in paragraph 1 of Article 16.1 of the OSAGO Law are met by the plaintiff only in relation to the claim for insurance payment.

Compliance with the mandatory pre-trial procedure for resolving a dispute provided for in paragraph four of clause 21 of Article 12 of the Law on Compulsory MTPL in order to apply to the court with claims for the recovery of a penalty and / or financial sanction is mandatory if a court decision that has entered into legal force considered the claim for payment of insurance compensation, and the claims for the claimant did not declare the collection of the forfeit and financial sanctions.

54. The amount of financial sanction for failure to comply with the deadline for sending a motivated refusal to receive an insurance payment to the victim is determined at the rate of 0.05 percent for each day of delay from the maximum insured amount according to the type of harm caused to each victim, established by Article 7 of the Law on MTPL (third paragraph of clause 21 of Article 12 Of the Law on MTPL).

The financial sanction is calculated from the day following the day established for making a decision on the payment of insurance compensation, and until the day of sending a reasoned refusal to the victim, and if it is not sent, until the day it is awarded by the court.

55. The amount of the penalty for failure to comply with the deadline for the insurance payment or compensation for damage caused in kind is determined at the rate of 1 percent for each day of delay from the amount of insurance compensation payable to the victim for a specific insured event, minus the amounts paid by the insurance company on a voluntary basis in the terms established by article 12 of the Law on MTPL (second paragraph of clause 21 of article 12 of the Law on MTPL).

The penalty is calculated from the day following the day established for making a decision on the payment of insurance indemnity and until the day the insurer actually fulfills the obligation under the contract.

56. The insurer shall be liable for non-fulfillment, improper fulfillment of obligations for the restoration of a damaged vehicle, including for violation of the terms of such repairs (paragraph 17 of Article 12 of the Law on MTPL).

The penalty for violation of the deadline for issuing a referral for restoration repairs or for violation of the deadline for performing such repairs is calculated from the amount of the insurance payment determined in accordance with Article 12 of the Law on Compulsory Motor Third Party Liability Insurance.

57. The collection of a forfeit along with a financial sanction is carried out in the event that the insurer violates both the time period for sending a motivated refusal to receive an insurance payment to the victim, and the time period for making an insurance payment or compensation for damage caused in kind.

It should be borne in mind that paragraph 6 of Article 16.1 of the Law on MTPL establishes a limitation on the total amount of penalties and financial sanctions collected by the court only in relation to the victim - an individual.

58. The insurer is released from the obligation to pay a forfeit, the amount of a financial sanction and / or a fine, if his obligations are fulfilled by him in the manner and within the time limits established by the Law on MTPL, and also if the insurer proves that the violation of the terms occurred due to force majeure or as a result of the guilty actions (inaction) of the victim (paragraph 5 of Article 16.1, paragraph 3 of Article 16.1 and paragraph 3 of Article 16.1 of the Law on MTPL is recovered in favor of an individual - the victim.

If the court satisfies the requirements stated by public associations of consumers (their associations, unions) or local government bodies in defense of the rights and legitimate interests of a specific victim - consumer, fifty percent of the amount of the fine determined by the court shall be collected by analogy with paragraph 6 of Article 13 of the Law on the Protection of Consumer Rights in the benefit of these associations or bodies, regardless of whether they have made such a claim.

If the court satisfies the claims of legal entities, the specified fine is not levied.

63. The presence of a litigation on the recovery of insurance compensation indicates the failure of the insurer to pay it on a voluntary basis, in connection with which the satisfaction of the victim's claims during the period of consideration of the dispute in court does not exempt the insurer from paying a fine.

64. The amount of the fine for failure to voluntarily fulfill the claims of the victim is determined in the amount of fifty percent of the difference between the amount of insurance compensation payable to the victim for a specific insured event and the amount of the insurance payment made by the insurer on a voluntary basis. At the same time, the amount of the forfeit (penalty), financial sanction, monetary compensation for moral damage, as well as other amounts that are not part of the insurance payment, are not taken into account when calculating the amount of the fine (paragraph 3 of Article 16.1 of the Law on MTPL).

65. The application of Article 333 of the Civil Code of the Russian Federation on the reduction of a penalty by a court is possible only in exceptional cases when the penalty, financial sanction and fine to be paid are clearly disproportionate to the consequences of the breached obligation. Reduction of forfeit, financial sanction and fine is allowed only at the request of the defendant. The decision must indicate the reasons why the court considers that the reduction in their size is permissible.

66. The forfeit, financial sanction and fine provided for by the Law on MTPL are also applied to the professional association of insurers (paragraph three of clause 1 of Article 19 of the Law on MTPL).

Related Articles